Sky-high prices, today’s mortgage rates, property taxes on those sky-high prices, and spiking homeowners’ insurance costs create a peculiar situation that more and more people are taking advantage of.

By Wolf Richter for WOLF STREET.

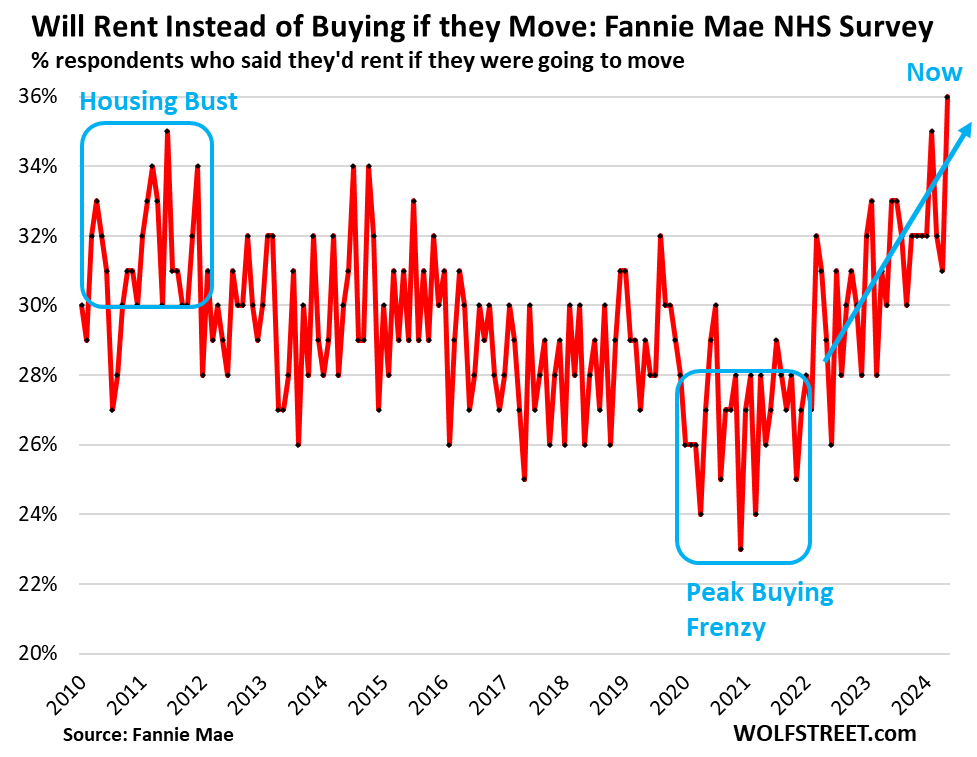

The share of people who said that they would rent rather than buy a home if they were to move spiked to 36%, an all-time high in the data going back to 2010, according to Fannie Mae’s National Housing Survey, up from the 23% to 28% range during the free-money buying frenzy in 2021-2022.

That 36% share has surpassed the highs of 2010 and 2011 during the housing bust, as home prices were in freefall. And the trend (blue arrow in the chart below) is promising to make renting an even more popular choice because it makes financial sense.

This is just another indication that the 50% explosion of home prices since 2020 – more in some markets, less in others, fueled by reckless monetary policies through 2021 – has created a peculiar situation where on a monthly cost basis, it is now far more expensive to buy a home than to rent an equivalent home pretty much across the country. And people are figuring this out, and they’re starting to engage in an arbitrage to take advantage of a price difference between similar products.

“One effect of the prolonged period of relatively high home prices of the past four years is that we are seeing a slowly growing preference to rent rather than buy on consumers’ next move,” Fannie Mae said.

“With rent growth expected to remain modest in 2025, more consumers may be seeking – and finding – attractive deals in the rental market as they continue saving toward a future home purchase,” Fannie Mae said.

But it’s not just too-high prices. Mortgage payments at today’s rates, for homes at today’s sky-high prices, plus property taxes on those sky-high valuations, plus skyrocketing homeowners’ insurance have seen to it that the monthly costs of buying a home today have far outrun the monthly worry-free costs of renting.

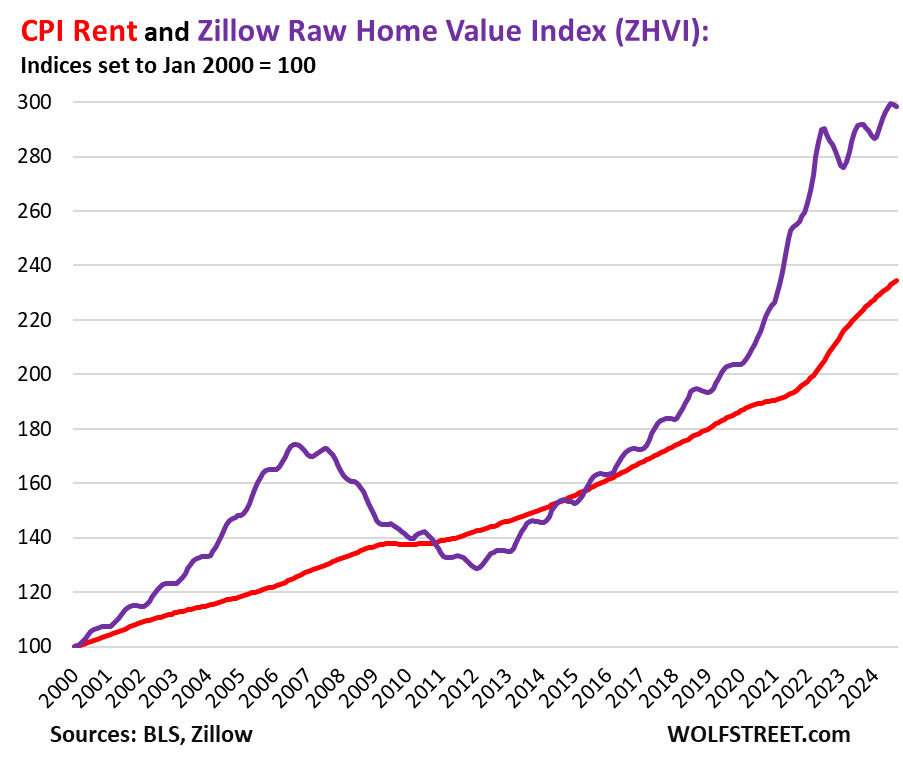

Simply comparing the trajectories of rents and home prices – excluding the effects of higher mortgage rates, soaring property taxes, and spiking homeowners’ insurance premiums – shows just how far home prices have gone out of whack.

For this purpose, we’re looking at the Consumer Price Index for Rent of Primary Residence via the Bureau of Labor Statistics’ CPI data (red) and home prices via Zillow’s “raw” Home Value Index data (purple) both set as index where January 2000 = 100.

And we see that rents have also surged, but not nearly as much as home prices. Again, this measure of home prices excludes the additional homeownership costs of higher mortgage rates, soaring property taxes, and spiking homeowners’ insurance premiums.

People are doing some basic math and are finding out that they’re getting ripped off if they buy an existing home now. If they buy, they will just make the sellers and Realtors rich, feed investors’ interest income from MBS, stuff local government coffers, and fatten up the revenues and profits of insurance companies.

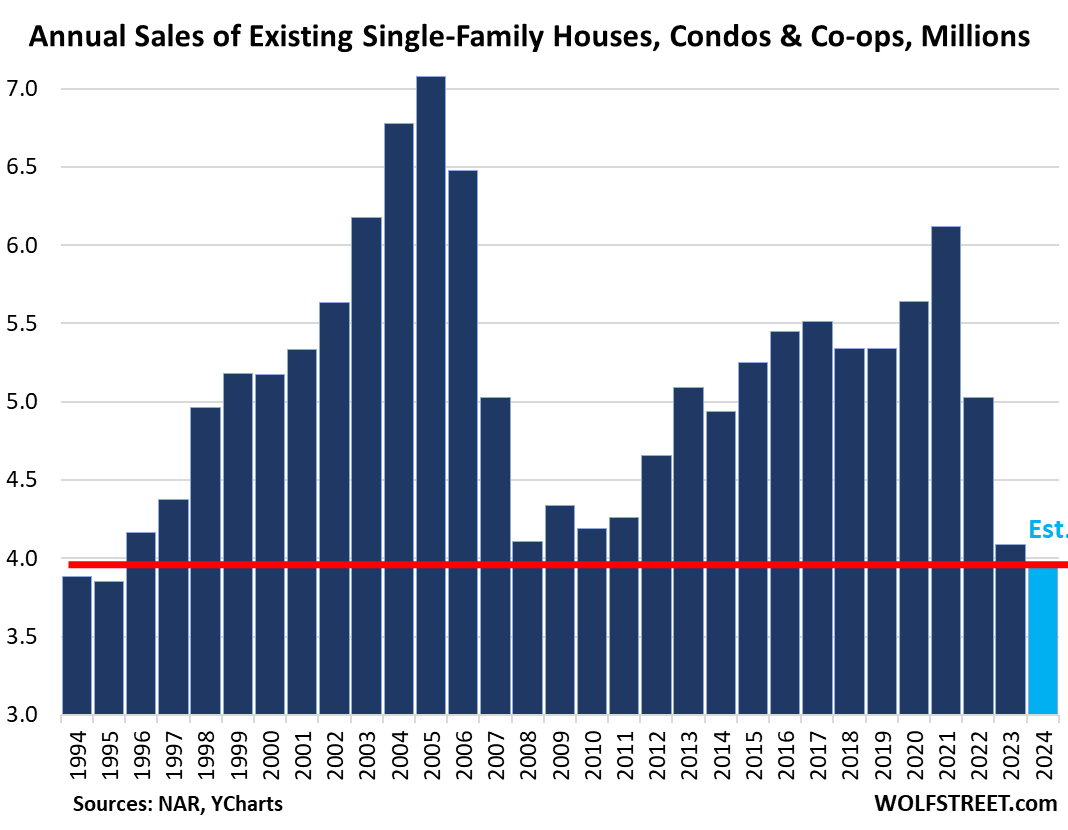

As more and more people have engaged in this arbitrage to take advantage of a price difference between similar products (renting v. buying a similar home), demand for existing homes has plunged to the lowest levels since 1995.

As demand has plunged, inventories and supply of new houses and existing homes have spiked, see the charts in the comments below.

And this growing preference for renting instead of buying will sap demand for home purchases even more, with sales having already plunged to levels not seen since 1995. Too-high prices destroy demand, which is a fundamental economic principle that even home sellers cannot escape (light-blue column = our estimate for 2024, historical data from YCharts).

If people rent a similar home, rather than buy it, they have more flexibility at a much lower monthly cost, they can save and invest this money or spend it, and they won’t be house-poor.

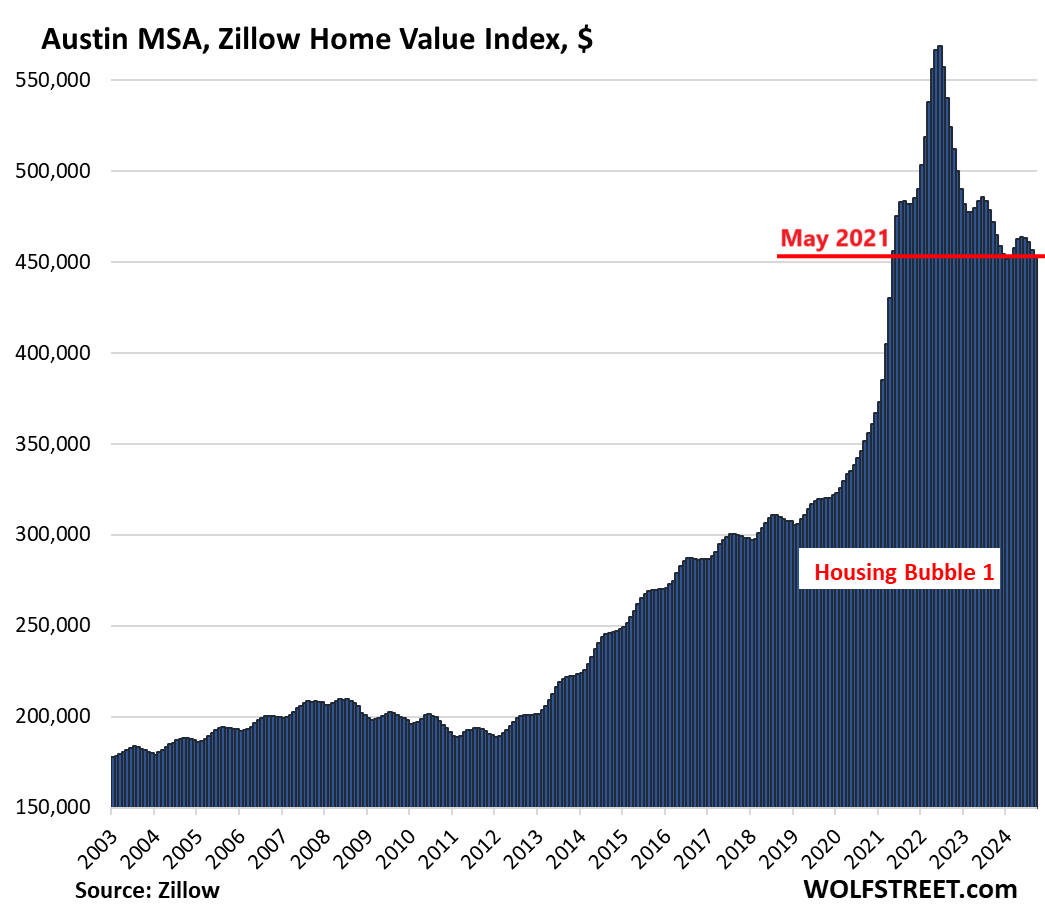

And with home prices now being targeted by higher mortgage rates and $2 trillion of QT so far – QT is in part responsible for those higher mortgage rates – these renters who choose to rent instead of buying have no risk of losing additional money when property prices head south, which they have already started doing in some markets, from our Most Splendid Housing Bubbles in America:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Energy News Beat