Trump explained it clearly yesterday, and markets understood. But companies have known it all along.

By Wolf Richter for WOLF STREET.

Stocks tanked today as markets understood what tariffs actually are: A tax on corporate profit margins that companies will have a very hard time passing on, which is why companies hate tariffs so much. If they could pass them on easily, they wouldn’t care about tariffs; their revenues would go up by the amount of the tariffs, and their profit margins in percentage terms could be maintained, and their stocks would keep rising. But that’s not the case.

Companies have known this all along. Markets figured it out today.

The S&P 500 fell 4.84% today. Markets have been so spoiled. Despite the decline of 12% from the high, the S&P 500 is still up 4.8% year-over-year, and by 31% from two years ago.

The Nasdaq fell 5.97% today and is down 18% from the high. But it’s still up 3.1% year-over-year, and by 37% from two years ago.

Stock-price gains have been so huge for so long that these declines are practically minor. Stocks have been at such precariously high levels that any little thing would knock them off their perch.

Longer-term treasury securities rallied, and yields fell, with the 10-year yield dropping to 4.03%, a classic safe-haven trade.

Trump explained tariffs yesterday, and markets understood.

President Trump outlined the new strategy of imposing layered tariffs on corporate profit margins yesterday in the Rose Garden, and encouraged companies to dodge those tariffs by shifting production to the US.

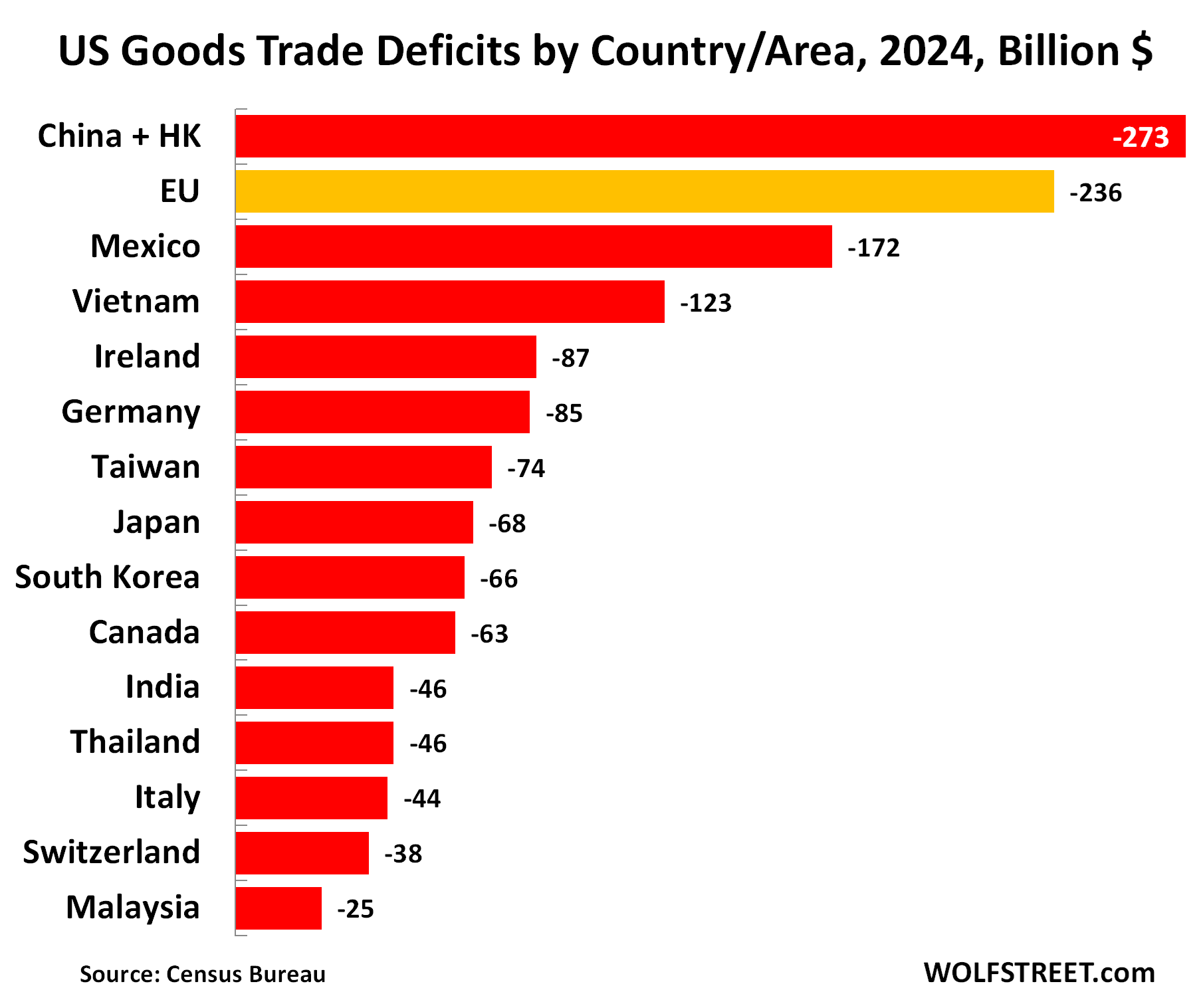

One of the countries he singled out was Ireland, where US Big Pharma companies have set up entities that make profits that are taxable under the low corporate income tax rates in Ireland, but are not taxed by the US. And then they sell those products in the US without profit, thereby dodging corporate income taxes in the US. Not paying income taxes in the US has widened the already big-fat profit margins of Big Pharma.

Other companies are doing the same thing. And so the US had this huge $87 billion trade deficit in goods with tiny Ireland last year, and Trump outlined how tariffs would change the math for this strategy.

The #1 goal of tariffs is to bring production to the US and end the system of “globalization at the expense of the US economy.”

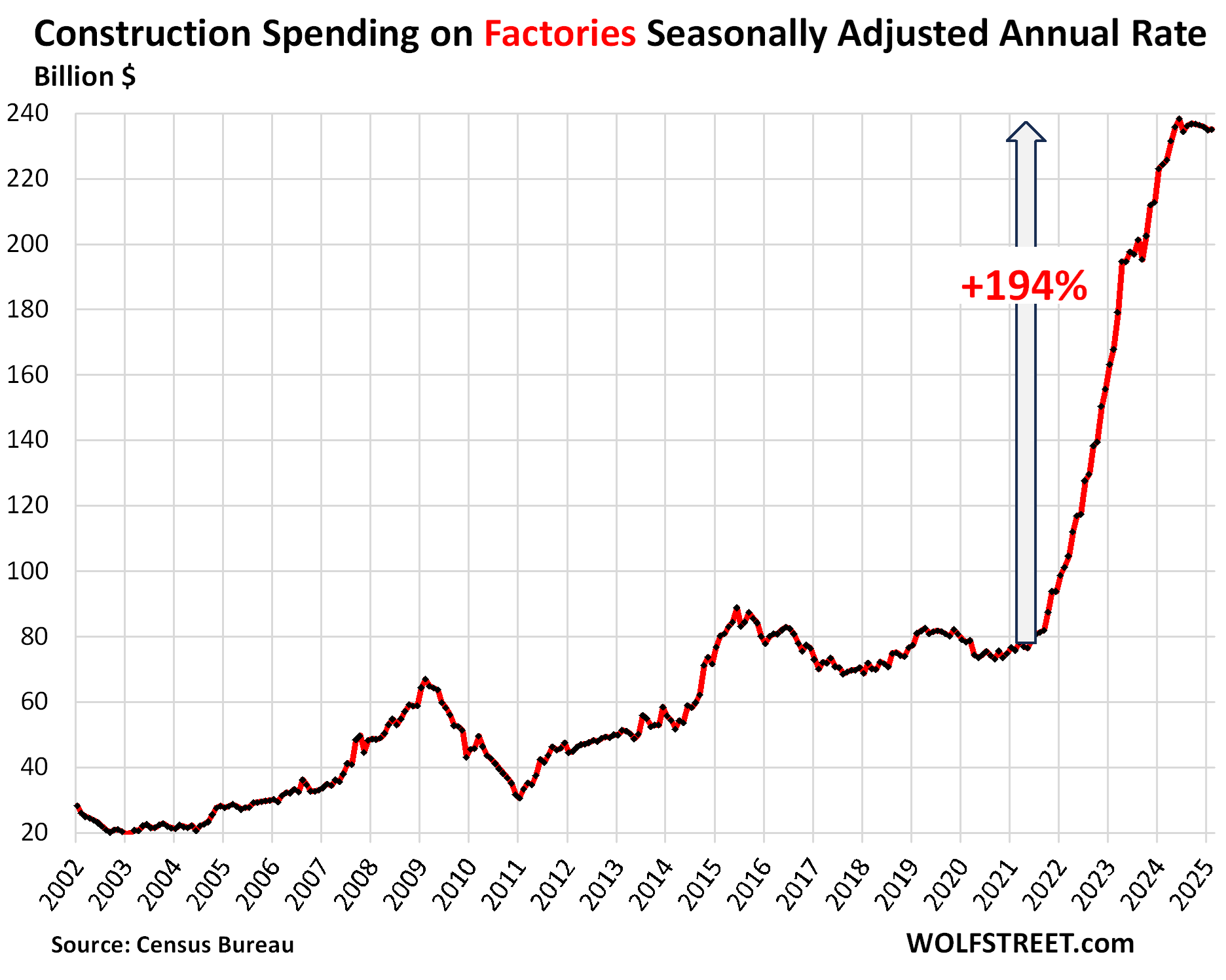

The entire auto industry has already been expanding and building factories in the US in recent years. Recently, numerous automakers have announced plans to build more factories in the US and produce more vehicles and components in the US. Same in the semiconductor industry and other industries.

It takes years to plan a factory, make a deal with local governments, buy the property, build the plant, equip the plant, and ramp up production, so this is not a short-term thing. All new factories in the US are highly automated, and employees are highly qualified, many of them are engineers.

The prior Trump tariffs were finalized in late 2018, after numerous changes, exemptions, carveouts, etc. By 2019 companies strategized and decided on how to deal with them long-term, including by planning to build factories in the US. Then came Covid in early 2020, and this process was put on hold. But in mid-2021, after the economy reopened, the first projects put all their ducks in a row, and the spending on the construction of factories started to soar, and it was the beginning of a historic construction boom.

This was further powered by the Biden Administration’s incentives. The CHIPS Act was passed in August 2022, and the first funds started flowing at the end of 2024.

And now come the new incentives to build factories in the US – in form of the new tariffs.

This is a hugely important development for the long-term strength of the US economy. Starting up a factory is a massive investment with immediate and long-term benefits for the US economy, including secondary and tertiary benefits.

The chart below shows this boom of the amounts spent on construction of manufacturing facilities. But they do not include the investments in equipment, such as industrial robots, computers, etc. that dwarf the construction costs of the building.

The #2 goal of tariffs is to impose taxes on corporate profits if companies decide to import, which forces companies to pay taxes that they might otherwise have dodged, such as Big Pharma and Big Tech that run their profits through Ireland and other financial centers and pay zero income taxes in the US on those profits sheltered overseas. Trump explained that yesterday, which may be why Apple tanked 9% today.

Tariffs are bad for stocks because they’re tax on corporate profit margins.

We know that, based on how stocks got hit in 2018 through the tariffs finally imposed then, and the S&P 500 went down 20%. I said in the headline on February 3: “What Trump’s Tariffs Did Last Time (2018-2019): No Impact on Inflation, Doubled Receipts from Customs Duties, and Hit Stocks”

Tariffs are bad for stocks because they extract taxes from companies, many of which would otherwise not pay income taxes in the US. Hence lower stock prices. The market understands that now just fine, despite the relentless BS in the media that tariffs are sales tax for consumers.

Passing on higher costs to consumers is very hard. It tends to cause sales to plunge, as Americans hate higher prices. And then, with sales dropping, the price increases are rolled back.

The Trump administration is refusing to let the addiction to inflated stock prices dictate essential long-term US economic policies. And markets are figuring it out.

Services exports don’t compensate for imports of manufactured goods. Services exports of the US fall mostly into two categories:

- Foreign tourism in the US – the money foreigners spend on lodging, restaurants, rental cars, airfares, etc., which are fairly low-level activities, unlike manufacturing of high-value goods, such as cars or semiconductors.

- Sales overseas of IP, such as software, movies, etc., that has already been made for and sold in the US, and whose sales in other countries add profits for the selling companies but create little or no additional economic activity in the US. Which is why services exports don’t have a lot of effect on the US economy, unlike manufacturing.

In addition, the services surplus the US has is small compared to the gigantic deficit in goods.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Energy News Beat