Driven largely by non-housing services. Just in time for the Fed meeting.

By Wolf Richter for WOLF STREET.

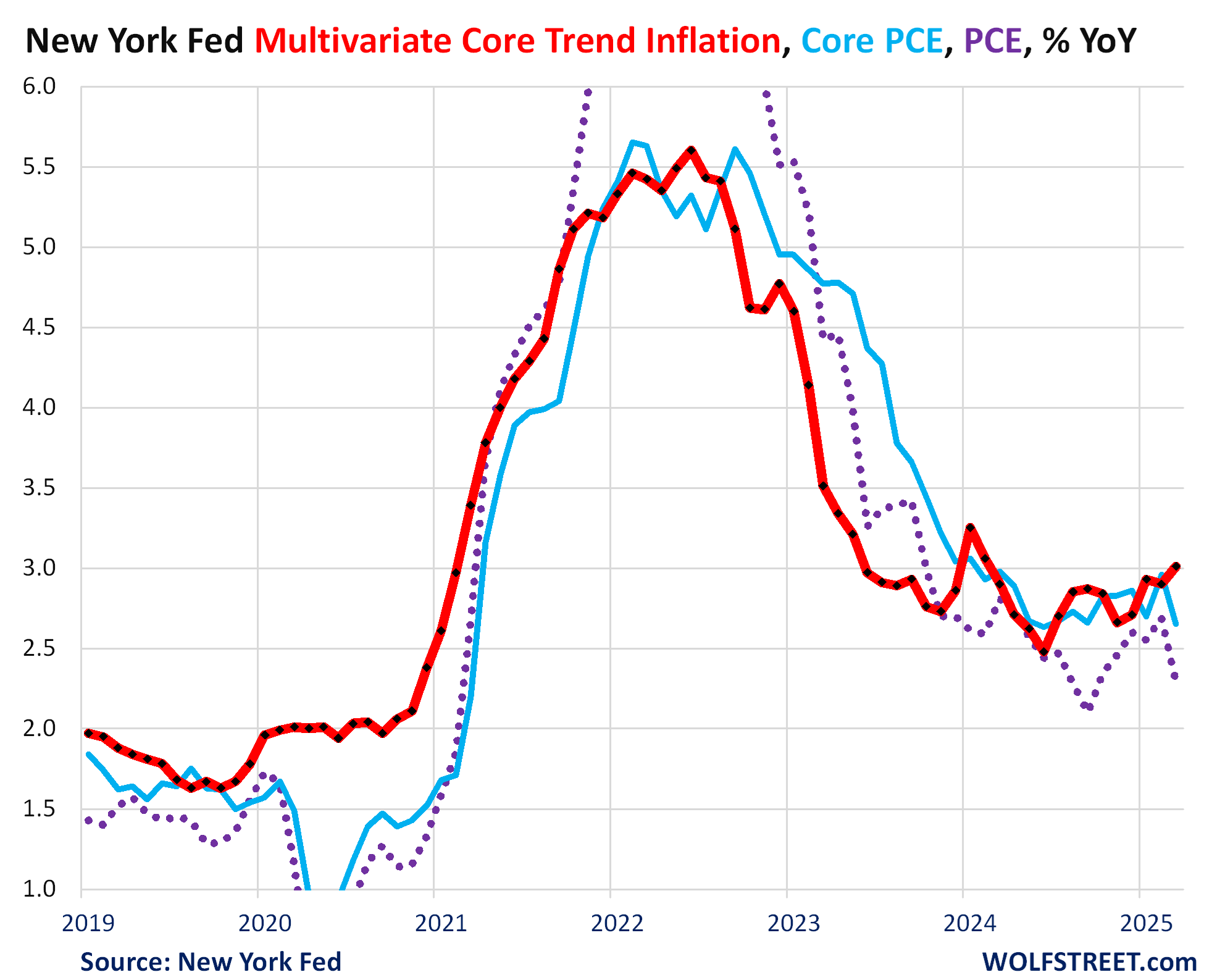

Back in April 2022, when the Fed’s favored inflation measure, the PCE price index, was surging towards its June 2022 high of 7.2% year-over-year, and core PCE to a high of 5.6%, the New York Fed came out with an inflation measure to track inflation’s “persistence.”

This “Multivariate Core Trend” (MCT) inflation measure is based on the some components of the PCE price index, but aggregates them differently. This MCT inflation rate, on a year-over-year basis, decelerated sooner than the core PCE and overall PCE inflation measures in 2022 and 2023, in effect successfully predicting their deceleration months in advance. And now it is predicting the resurgence of PCE inflation.

The MCT inflation rate for March accelerated to 3.0% year-over-year, the worst reading since February 2024 (red in the chart), according to the New York Fed today. The re-acceleration was driven largely by non-housing services and to a small extent by “core goods” components, even as the Fed-favored core PCE inflation (blue line) and overall PCE inflation (purple dots) decelerated year-over-year (my discussion of PCE inflation for March).

So now MCT, which attempts to show “persistence” of inflation, is predicting a substantial re-acceleration of inflation – the “persistence” part – driven largely by non-housing services and to a small extent by core goods. So housing cost inflation, as measured by rents, is no longer the driver of this inflation; it’s non-housing services and to a small extent, core goods.

Should we take this MCT seriously, after it was designed to run ahead of the surge of inflation in late 2020 and early 2021, and then successfully predicted the deceleration of core PCE and PCE inflation in 2022 and 2023?

In this inflation whack-a-mole, where inflation pressures shift to different products and services all the time, anything that can shed light on inflation’s next move – such as the concept of “persistence” in inflation – helps.

These kinds of data points are precisely why the Fed pivoted to wait-and-see. The inflationary pressures evident in the MCT inflation measure, especially in services, have not been impacted by tariffs. Whatever portion of tariffs might seep into consumer prices — instead of getting hung up in the record fat corporate profits that resulted from huge price increases during the free-money era — would still come on top of it.

Consumers hate hate hate higher prices, and now that the free money has vanished, they’re resisting further price increases on top of the already very high prices. Companies hike prices, consumers stop buying the product, price increases have to be rolled back to maintain sales. A slew of major companies have already conceded to investors that they would have to eat the tariffs this year. So passing on tariffs will not be easy. But whatever portion will seep into consumer prices could become persistent, rather than just a one-time bump: that’s another worry Powell has mentioned.

The Fed will meet on Tuesday and Wednesday, and will release its statement on Wednesday afternoon, and Powell will talk afterwards at the FOMC press conference, and there will be fretting over this “persistence” of inflation, and the potential for inflation to accelerate further this year, and the Fed apparatus will lean against the incessant demands for rate cuts.

We give you energy news and help invest in energy projects too, click here to learn more

Crude Oil, LNG, Jet Fuel price quote

ENB Top News

ENB

Energy Dashboard

ENB Podcast

ENB Substack

The post NY Fed’s “Multivariate Core Trend” Inflation Measure Hits 3.0%, Worst in Over a Year, Predicts Acceleration of PCE Price Index appeared first on Energy News Beat.

Energy News Beat