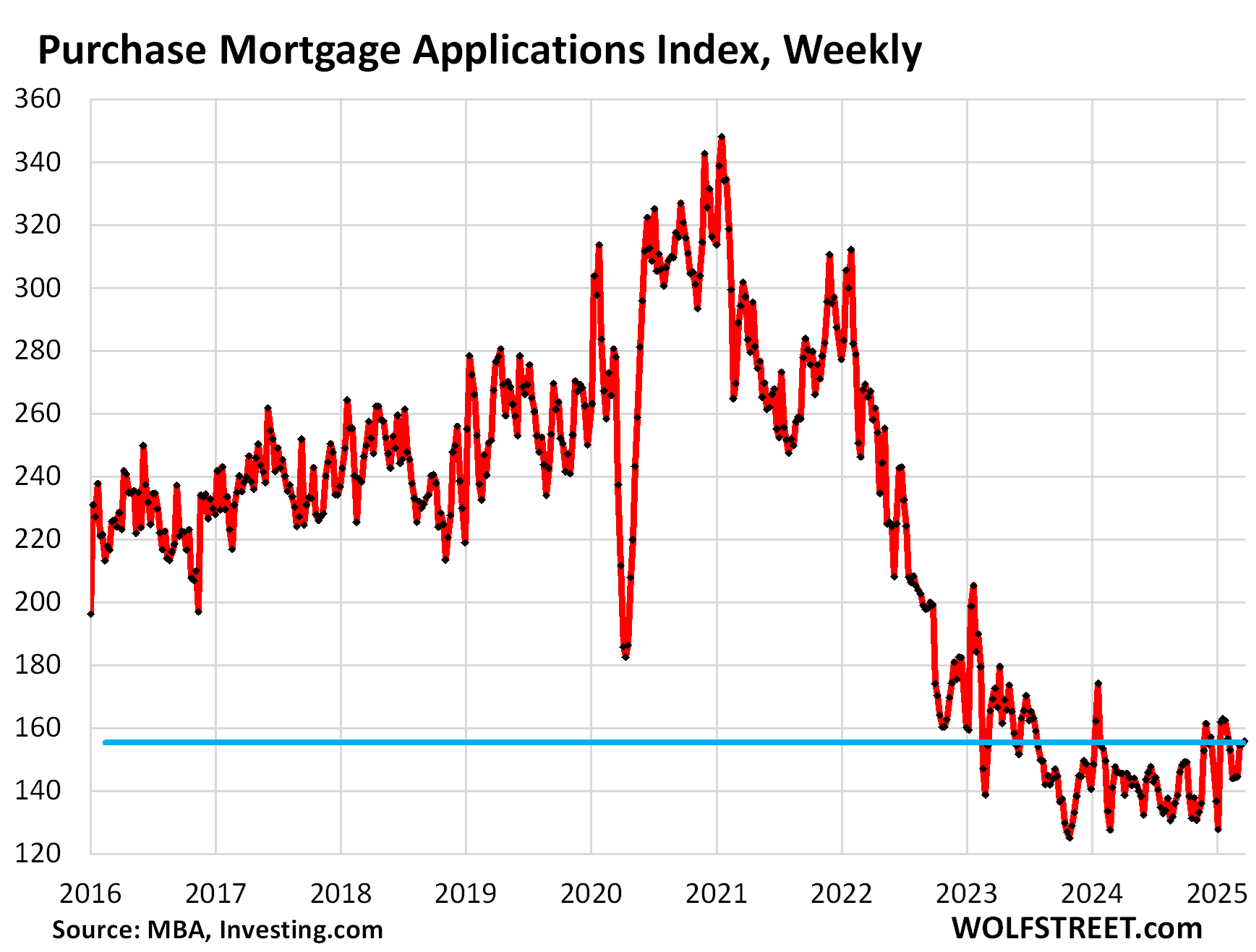

Demand for mortgages to purchase a home has plunged by nearly double the rate of sales of existing homes.

By Wolf Richter for WOLF STREET.

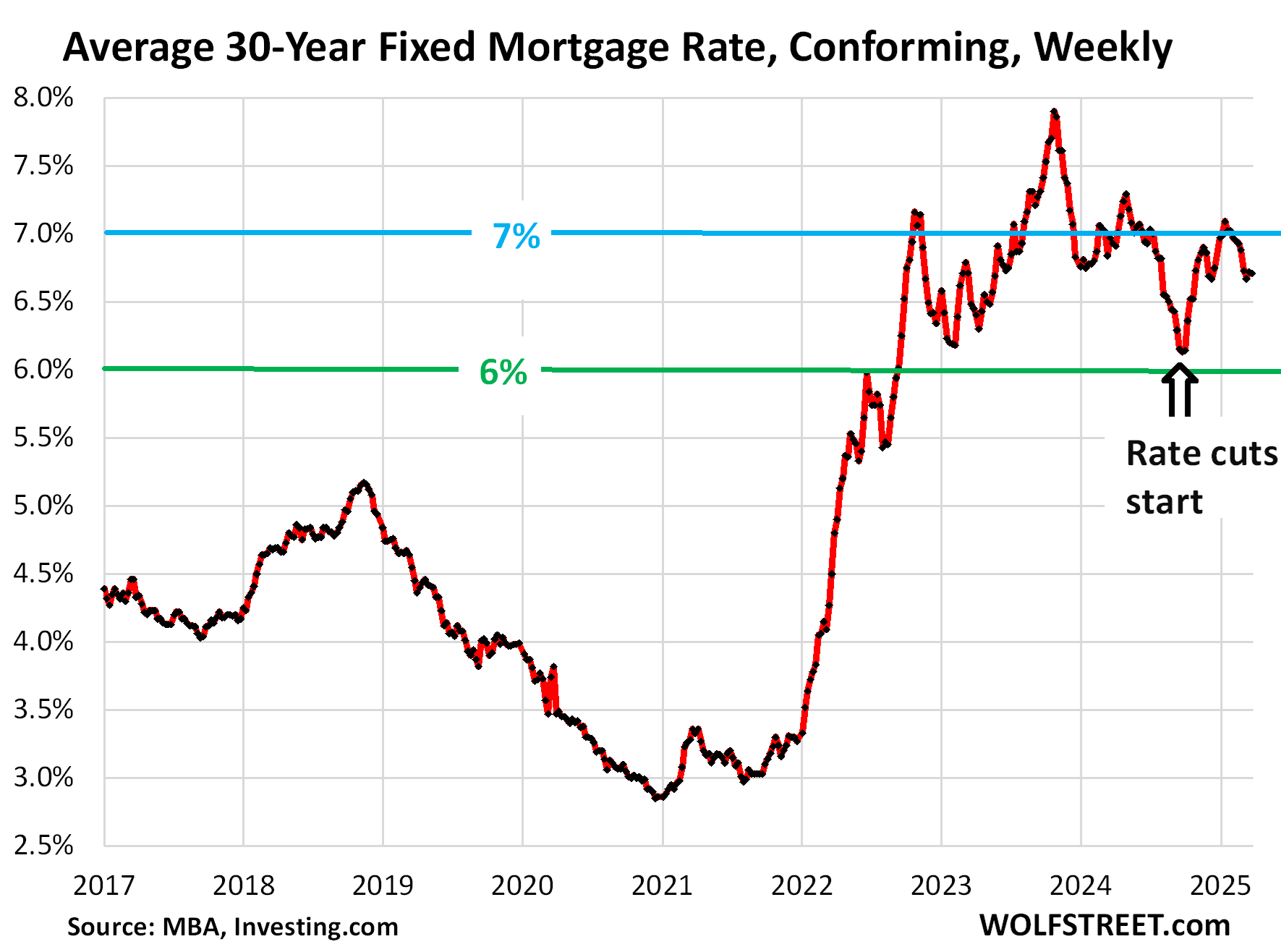

For the past four weeks, mortgage rates have stabilized at just over 6.7%, with the average conforming 30-year fixed mortgage rate ticking up to 6.71% in the latest week, according to the Mortgage Bankers Association today.

The combination of what were normal-to-low mortgage rates in the pre-QE era before 2009 and the fantastical prices today, after the huge QE-fueled run-up in recent years, has whacked demand: Sales of existing homes plunged by 24% last year from 2019, and this year doesn’t look much better, with February having been the worst February since 2009.

But demand for mortgages to purchase a home has plunged by nearly double the rate of sales of existing homes: by 42% from 2019.

Between mid-September and mid-December, the Fed has cut its short-term policy rates by 100 basis points, just as inflation had started to re-accelerate. A dovish Fed in face of rising inflation spooked the long-term bond market, and long-term yields shot up, including mortgage rates.

The MBA’s measure shot up by nearly 100 basis points, while the Fed cut 100 basis points, widening the spread between the two by 200 basis points.

The market essentially told the Fed that was considering further rate cuts in this inflationary environment: “Go ahead, make my day!”

Did the market teach the Fed a lesson, that cutting rates in an inflationary environment can push up long-term rates, fast? At any rate, it turned hawkish, putting further rate cuts on hold and talking tough on inflation, and long-term yields eased off a bit, but not much, and after the initial drop, mortgage rates have been hung up at 6.7% for the fourth week in a row:

Mortgage applications to purchase a home have been wobbling along since October 2022 not much above the record lows of November 2023 and then again of February 2024 (the data goes back to 1995).

In the most recent week, they ticked up a hair and were up by 6.9% from a year ago, which had been near the record-low of February 2024. Compared to the same week in 2019, purchase mortgage applications were down 42%.

This 42% plunge in purchase mortgage applications documents to what extent the housing market remains frozen because prices are still too high and buyers have gone on strike – though prices have started to come down in a number of markets.

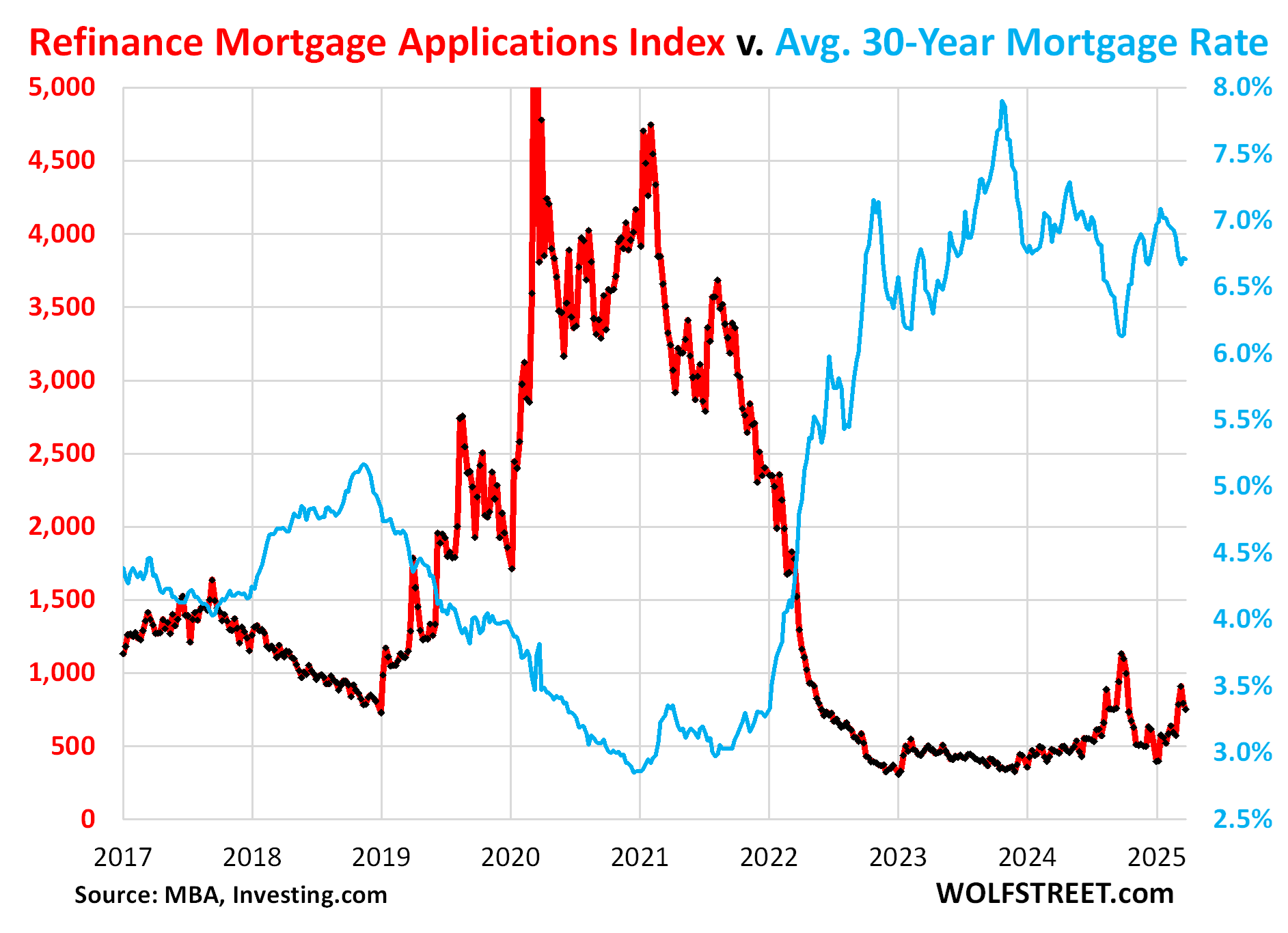

Mortgage applications to refinance a home began collapsing spectacularly when mortgage rates started rising in 2022, following the huge boom during the 2.5%-3.0% mortgage-rate era.

But people still need to do refis for various reasons, including to draw cash out of the home, and interest rates on refis are lower than rates on HELOCs or other types of loans. So the refi business has picked up some, having roughly doubled from the low point in early 2023, but remains at depressed levels.

In the latest reporting week, refis were up 49% year-over-year, but still down by 42% from the same week in 2019, and by 77% from the same week in 2021.

This chart illustrates the inverse correlation between mortgage refis (red) and mortgage rates (blue).

And yet, supply has surged to the highest in years. Supply of unsold existing homes on the market in February, at 3.5 months, was the highest for any February since 2019, and higher than in February 2018.

In terms of new single-family houses for sale: Inventory has surged to the highest since the peak of the housing bust, and in the South has been above the peak of the housing bust for months.

So buyers remain on strike. They’re waiting for prices to come down, and they’re waiting for rates to come down, though in an inflationary environment, that may not happen to the extent they’re hoping for.

And while they’re at it, they’re waiting for their household incomes to rise, and in the current inflationary environment, that’s happening faster than in the prior decades, but it will take years before it makes any significant difference. So the buyers’ strike, already in its third year, may last a while longer.

But a combination of lower prices and higher incomes would work wonders over the years in helping the housing market get over the ridiculous QE-fueled price spike and return to some form of normality.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The post Home Buyers Still on Strike, Waiting for Lower Prices, Lower Rates, and Higher Incomes appeared first on Energy News Beat.

Energy News Beat