Source: Zero Edge

Authored by Alasdair Macleod via GoldMoney.com,

The increasing number of nations seeking to join BRICS brings geopolitics into the spotlight. At the time of writing, existing members, those who have applied to join and those expressing an interest total 36 nations, with over 60% of the world’s population and one-third of global GDP.

Plans for a new trade currency backed by gold appear to be on the agenda for the BRICS meeting in Johannesburg in August. In this article, the geopolitical aspects of its introduction are considered, and the indications that how it will involve gold are discussed. The mechanics of this project are then suggested.

But first, we look at the situation in Ukraine, attempting to put the recent Wagner rebellion into context. Furthermore, Russia’s deteriorating trade surplus, weakness of the rouble and rising bond yields suggest that it is time for President Putin to put an end to Ukraine’s misery. He is likely to do this by attacking Kiev, which is only 60 miles from Belarus, while the bulk of Ukraine’s army is distracted by operations over 400 miles to the south and east.

Introduction

Given the hysteria in the Western press over the Wagner group’s alleged coup attempt, it is time for an update on the battle between the hegemons. But I shall commence with an attempt to put the leader of the Wagner mercenary group’s supposed coup attempt to bed.

It emerges that Western intelligence knew something was up, as much as ten days before the dispute between Wagner and the Russian defence ministry became evident. This was The Daily Telegraph yesterday:

“Before Wagner troops began their advance on Rostov and then on to Moscow last weekend, British officials had ‘an extremely detailed and accurate picture of the mutiny plans’, it was revealed yesterday. The details were shared by US intelligence ahead of the mutiny and contained information of where and how Wagner mercenaries planned to move.”

This immediately puts up a red flag. Did Britain’s MI6 or the CIA have a part in it? If not, how is it that they knew so much about it? Is it likely that the Wagner leadership or elements in it had been bribed by western intelligence into staging an attempted coup of the Russian government? But we must leave this speculation hanging, in the certainty that black ops are being widely deployed by western intelligence in Ukraine, Russia, and Belarus and that anything is possible.

Western commentary, always informed by government briefing and censorship, seems to take Putin for a fool. We are routinely told in op-eds that his regime hangs by a thread, the Russian economy is in a state of collapse, and similar episodes to the Wagner farce have always been the straw about to break Putin’s back. It has been going on like this since the launch of his special military operation in February 2022. If he smoked, like Castro doubtless the CIA would offer him a box of exploding cigars.

But clearly, Putin is no fool. He will realise the limitations of mercenary troops. He has used Wagner specifically to spread fear in Eastern Ukraine. Like the French Foreign Legion of Beau Geste yore, Wagner’s recruiting ground appears to have been among jailbirds, criminals on the run, social misfits, and is a haven for psychopaths.

It seems that Prigozhin’s complaint (who leads the Wagner force) was not with Putin but his senior military advisers. There is a long history of commanders in the field being frustrated with ministerial ineptitude. To Prigozhin, it is likely that Wagner’s role in Eastern Ukraine had evolved from clear military objectives to a feeling of being hung out to dry, while Russian divisions led by inept generals dithered. Putin would have understood why Prigozhin threw his toys out of the pram and sought to calm him down. Furthermore, Putin’s special military operation is probably entering a new phase where mercenary forces might complicate battlefield planning, as I shall explore further in this article.

Undoubtedly, Wagner’s role will continue to be countering American and British undercover activities in foreign theatres such as Kurdistan, Chad, and Sudan. And the majority of his forces in the Ukraine theatre will probably be absorbed into the Russian army as Putin’s special military operation enters a new phase. And if Prigozhin managed to get a backhander out of the Americans to “stage a coup d’état” as conspiracy theorists suggest, I suspect that this comic opera will end up with both Prigozhin and Putin enjoying the joke at the western alliance’s expense.

Russia’s situation

We were originally told that sanctions would rapidly bring Russia to her knees and force the Russian people to overthrow Putin. Neither have materialised, and the evidence is that the Russian economy is stronger today than it was a year ago and Putin’s public backing remains high. Since early-2022, Russia’s economy had officially been in a mild recession, but in April economic activity was recorded as rising sharply due to buoyant industrial production and retail sales.

Sanctions never work, and a sanctioned nation rapidly adapts. Furthermore, while sanctions have focused on hitting Russian oligarchs, a low flat 13% income tax and corporation tax of 20% on company profits means that Russian SMEs, artisans, and shopkeepers are doing well. It also explains Putin’s continually high approval ratings, but Russia’s economy has far greater potential under sound money and lower interest rates. Furthermore, with consumer price inflation running at about 2.5%, domestic economic conditions are remarkably stable.

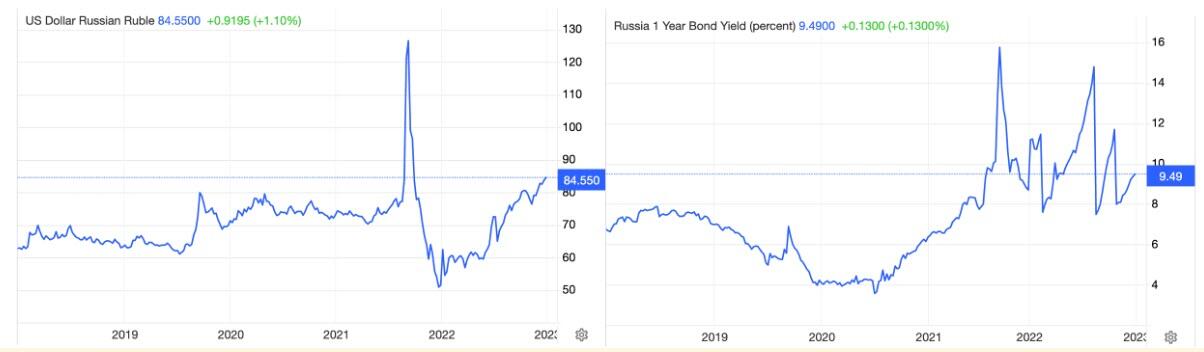

Russia’s balance of payments has been declining sharply. According to the central bank, the current account surplus between January and May was $22.8bn equivalent, compared with $123.8bn for the same period last year. This decline was due to lower oil and commodity prices, as well as marginally lower export and higher import volumes. The rouble has declined, and interest rates have recently risen as the charts below illustrate.

{kind=link}

To have such volatility in the exchange rate and interest rates is the greatest weakness in Russia’s economic condition. The way to fix it is for the rouble to adopt a proper gold standard. And between the Bank of Russia’s official gold reserves, Russia’s National Wealth Fund, and the Gokhran precious metals fund there are ample bullion resources to establish it. The merits of such a move for the domestic economy would be interest rate stability at far lower rates. Bank credit could then respond to economic demand for credit, which would undoubtedly expand, without undermining the rouble’s domestic purchasing power.

Putin and his economic adviser, Sergey Glazyev, have shown that they understand these benefits, and that a gold standard for the rouble is likely to be Russia’s end game in the financial war against the western alliance. Furthermore, unless energy and commodity prices begin to increase, the fiat rouble and Russian interest rates could come under renewed pressure. The other way to look at rising energy and commodity prices is to attribute them to a decline in the dollar’s purchasing power for them, artificially suppressing their values.

This brings us to the reasons for Russia to step up the attack on Ukraine, which can be expected to give a new impetus to higher energy and commodity prices.

Besides the need to drive commodity prices higher for the benefit of the rouble and the balance of payments, the timing appears propitious. The redeployment of battle-hardened Wagner troops in Belorussia across the border from Kiev could form part of Putin’s plan for a new attack, now that Ukraine’s summer campaign to recover territory in the East and South is absorbing most of Ukraine’s military forces.

Before we were distracted by the Wagner episode, there were putative signs that the US deep state was changing its view from the conflict being easily winnable with covert support and Putin vulnerable to being toppled. And therefore, the true objective, the dismemberment of Russia, is no more than a dream and the proxy war is becoming a long drawn out operation. There is now little doubt that as a front man Zelensky is unable to deliver the goods, and his supporters in the western alliance are faced with being committed to the long haul.

The stakes for America are extremely high. Increasingly, neutral countries around the world are shifting their foreign policies on the evidence that America and her dollar are losing their hegemonic power. If America and NATO fail in Ukraine, it won’t just be thirty nations lining up to join BRICS: it will be the moment America’s political grip on the world is certainly lost. And then President Biden can kiss goodbye to his re-election chances next year.

Equally, Putin will strive to make sure his counteroffensive succeeds, and that must be the short-term priority. The financial benefits for Russia, principally the consequences for energy and oil prices will flow from it.

Russia is unlikely to immediately adopt a gold standard for the rouble when Ukraine falls because of the geopolitical consequences, not least for its partnership with China. It would undoubtedly hasten the fiat dollar’s destruction as a reserve currency, making financing of the US trade and budget deficits virtually impossible at current interest rates. While these outcomes would undoubtedly be helpful to Putin, it would amount to a major escalation of the financial war between Russia and the western alliance with unpredictable consequences. And it would be a change from Putin’s proven strategy of letting the western alliance make all the strategic errors without his intervention.

Furthermore, Russia is in partnership with China in a joint grand strategic plan for Asia and allied nations. And there is no doubt that the economic consequences of a collapsed dollar would rebound badly on China’s manufacturing base.

Far better to commence the move towards gold backing by other means, and this train of events has already been put in place under the command of Sergey Glazyev, a close confident of Putin, a moving light in the expansion of the Moscow Gold Exchange, and Minister in charge of Integration and Macroeconomics for the Eurasian Economic Commission. Glazyev was given the brief to come up with a new trade settlement currency for the Eurasian Economic Union (EAEU), which appears to be a Trojan horse for a wider BRICS and Shanghai Cooperation Organisation deployment.

If that plan is successful, then both the rouble and China’s renminbi could also adopt gold standards in due course, having the underlying financial conditions to sustain them.

The BRICS summit in Jo’burg

There is evidence that plans for a new trade settlement currency will be announced at the upcoming BRICS meeting in Johannesburg on 22—24 August[i]. If so, it will be a major development for global markets and a threat to the dollar’s future. And a new supranational trade currency for BRICS, the Shanghai Cooperation Organisation, and the Eurasian Economic Union has the merit of not having to address the vested trade and domestic currency interests of each member state. It would be designed to ensure its reserve status does not give overriding power to one nation, unlike the dollar.

It is probable that an announcement concerning the new currency will come out of the summit, but it is likely to be preliminary in nature, and gold might not even be mentioned at this stage. And it would make more sense for Glazev’s brief designing such a currency to be officially expanded from that of the EAEU committee, involving China more directly. That being the case, the only practical means of tying the new trade currency to multiple commodities and national interests is to use gold.

It increasingly suits Russia to see this move announced, and the timing could well coincide with or shortly follow Putin’s next push in Ukraine. But we should not expect this new currency to arrive shortly, only that it is being planned.

Another aspect of the Johannesburg summit is the increasing queue for BRICS membership. It will need the agreement of existing BRICS members. But given that the existing five members have diverse political interests, if is not easily forthcoming either China and Russia will have to strong-arm them into acceptance, or form a different membership category, such as associates. Either way, formal applications have been submitted from Algeria, Argentina, Bahrain, Bangladesh, Egypt, Indonesia, Iran, Saudi Arabia, and the United Arab Emirates. In addition, Afghanistan, Belarus, Comoros, Cuba, Congo, France, Gabon, Guinea-Bissau, Honduras, Kazakhstan, Nicaragua, Nigeria, Pakistan, Senegal, Sudan, Syria, Thailand, Tunisia, Turkey, Uruguay, Venezuela, and Zimbabwe have expressed an interest. Including the existing five members, that is 36 nations in total

The most interesting expression of interest comes from France, with President Macron reported to have applied to attend the Johannesburg summit. Only yesterday, it was reported that he was denied the opportunity to attend. But it is visible evidence of an EU member not toeing the American line. And recently, TotalEnergies the French conglomerate sold LNG to China for yuan, not dollars, signalling France’s independence from petrodollars.

Discounting France from actually applying for membership because Macron has his hands firmly tied by the EU, if membership was granted to all other applicants and those interested in joining an expanded BRICS, it would encompass 64% of the world population, and 33% of world GDP in 2017 (the latest year for which all individual national GDPs is available). For reference, the US’s population is 4.25% of global population and 24% of 2017 global GDP.

It seems to have escaped wider notice, but the only full members of the Shanghai Cooperation Organisation not members of BRICS, applying for membership, or expressing an interest are the four central Asian states — Kazakhstan, Kyrgyz, Tajikistan, and Uzbekistan, already in the EAEU. Furthermore, nine of the SCO’s Observer States and Dialog Partners are among the BRICS applicants. This is almost certainly centrally organised, with the possible objective for BRICS to be merged with the SCO, or to become indistinguishable from it.

For China and Russia, the advantages of integrating the SCO with BRICS are obvious. They are assembling an organisation based on free trade which dwarfs the US and EU and extends beyond Asia. Macron appears to be aware of the implications, and so are Germany’s industrial leaders, opening the way for an EU schism and an extension of Asian hegemony. It builds a trade bloc which makes the western alliance’s sanctions meaningless and will have complete independence from the dollar and its allied fiat currencies. Alternatives to the SWIFT international payments system now exist and can be easily extended.

It will allow for military and intelligence cooperation against terrorism (for which read Five Eyes’ black ops). In this, the experience of the Middle East has been instructive. Since Saudi Arabia sided with China and gave the US its marching orders, peace has been restored to the region.

The thinking behind a new trade currency

While any announcement about a new trade settlement medium at the BRICS summit in Johannesburg is likely to be preliminary, we can be sure that the legwork has already been done by Sergei Glazyev. Furthermore, various statements by nations prepared to accept settlement in national currencies other than the dollar must be seeing this as a temporary solution, pending more satisfactory payment arrangements. The Saudis accepting Kenyan shillings, or Russia accepting Iranian reals makes no sense on any other basis. Because the current position is temporary, it is time limited.

In an article entitled “Golden rouble 3.0: How Russia can change foreign trade infrastructure”[ii] written for Vedomosti, a Moscow-based Russian business newspaper published on 27 December2022, Glazyev laid out his latest thoughts. Furthermore, it was co-authored by Dmitry Mityaev, who is Assistant Member of the Board for Integration and Macroeconomics of the Eurasian Economic Commission — so this article was not just Glazyev’s musings, and we can assume that it carried official weight in Russia, at least. The article focused on the potential for a gold-backed rouble rather than the new trade settlement medium, but the same logic applies.

From this article, the EAEU currency commission now appears to have dropped the original indicated proposal for a new currency based on a weighted index of participating currencies and commodities entirely, using gold and credit based upon it instead as the principal means of settling trade imbalances. Presumably, the requirement to make payments in the new trade currency could be circumvented if one or more national currencies such as the rouble or renminbi went onto credible gold standards. The implication is that the rouble will readopt a gold standard sometime after a gold-backed trade currency is announced, reviving the gold backing (though not the relationship) that the Soviets operated between 1944 and 1961.

To reinforce the importance of a return to a gold standard, both Russia and the Saudis heading up OPEC+ will be aware of the consequences of the fiat petrodollar regime for their primary export product — crude oil.

In August 1971, when the Bretton Woods agreement was abandoned, crude oil was priced at $3.56 a barrel and the market price for gold was $42.85. Converting this into ounces of gold per barrel gives us a value of 0.0831 ounces. Today, the gold price of oil is 0.036 ounces per barrel, down 57%. In other words, using gold Glazyev can demonstrate that the true cost to OPEC+ of dollarisation has been to more than halve the value of their export revenues since the Bretton Woods agreement was suspended. By accepting a new trade settlement medium tied to gold, this US enforced erosion of oil values will cease. And to compensate for the loss of oil’s value from the ending of Bretton Woods, the gold price in dollars would have to be more than double that of today at over $4,400.

The evidence mounts therefore, that gold provides a framework within which Glazyev intends to operate. That he must be thinking this way has become fundamental to his approach, confirmed by his many references to gold in his article for Vedomosti, to the rouble’s history tied to gold, and to the US’s debasement of petrodollars. In the UK at least, Russia’s media appears to be censored, so Glazyev’s Vedomosti article (referenced in endnote ii) may not be available to many readers in the west. Therefore, for ease of reference the salient points in the English translation of his detailed article are summarised as follows [with additional commentary in square brackets]:

In the nine months to September 2022, Russia’s trade surplus with members of the EAEU, plus China, India, Iran, Turkey, The United Arab Emirates etc. was $198.4bn equivalent, against $123.1bn for the same period last year. In other words, the western alliance’s sanctions failed to suppress Russia’s oil revenues, merely redirecting their sources. [Since then, this surplus has declined materially due lower oil and other commodity prices. Time for another special military operation?]

The trade surplus with SCO members has allowed Russian companies to pay off external debts, replacing them with borrowing in roubles. [Glazyev doesn’t make this point, but a return to the gold standard would reduce borrowing costs in roubles substantially]

Russia became the third largest country using renminbi for international settlements, accounting for up to 26% of foreign exchange transactions in the Russian Federation. The share of settlements in soft currencies is growing for SCO members, dialog partners and associates, replacing dollars, and is expected to increase further. [This is almost certainly a temporary fix, ahead of a new trade settlement currency being established]

Since these currencies are subject to exchange rate risks and possible sanctions, the best way to offset them is to take payment in non-sanctioned gold from China, the UAE, Turkey, possibly Iran, and other countries instead of their local currencies. [A BRICS/SCO trade settlement currency tied to gold would eliminate this problem]

Gold purchased by the Russian Central Bank can be stored in central banks of friendly countries for liquidity purposes and the rest repatriated to Russia.

Gold can be a unique tool to combat western sanctions if used to price all major international goods (oil, gas, food, fertilisers, metals, and solid minerals). This would be “an adequate response to the west’s price ceilings”. And “India and China can take the place of global commodity traders instead of Glencore or Trafigura”.

Gold (along with silver) for millennia was the core of the global financial system, an honest measure of the value of paper money and assets… It was cancelled half a century ago, tying oil to the dollar. But the era of the petrodollar is ending. Russia, together with its eastern and southern partners has a unique chance to jump ship from a dollar-centred debt economy.

By signing the Bretton Woods agreement but not ratifying it, for the USSR “Golden Rouble 2.0” played an important role in post-war Soviet industrialisation. Now the conditions for “Golden Rouble 3.0” have objectively developed.

Sanctions against Russia have boomeranged against the west. It now faces geopolitical instability and rising prices for energy and other resources [i.e., yet more price inflation].

In 2023, [there will be a shift from] risky investments in complex financial instruments to invest in traditional assets, primarily gold. Gold’s increasing prices towards Saxo Bank’s forecast of $3,000 per ounce will lead to a substantial increase in the values and quantities of gold reserves. Large gold reserves will allow Russia “to pursue a sovereign financial policy and minimise dependency on external lenders”. [Note that in addition to official reserves it is believed that Russia has at least a further 10,000 tonnes — more than the officially declared total for the US Treasury.]

Central banks are adding to their gold reserves. China has an export ban on all mined gold. According to the Shanghai Gold Exchange, customers have withdrawn 23,000 tonnes of gold. India is considered the world champion in gold accumulation…. Gold has been flowing from West to East… Is the West’s central bank gold safely earmarked, or is it all “de-done” through swaps and leasing? The West will never say, and Fort Knox’s audit will not either.

Over the last 20 years, gold mining in Russia has almost doubled. Gold production may well grow from 1% of GDP to two or three per cent… Already, Russia’s annual gold production is set to rise from 300 tonnes to 500 tonnes… giving Russia a strong rouble, strong budget, and a strong economy. [Note that in this statement Glazyev reveals that he expects most of the increase of mine output is to be in its value measured in dollars.]

Glazyev is all but saying for definite that Russia plans to enact Golden Rouble 3.0. And we should be in no doubt that Russia is backing away from the west’s fiat monetary system and sees far higher gold prices expressed in falling dollars. The only question is the speed with which it is moving in this direction.

What Glazyev did not mention in his Vedomosti article, other than his reference to western central banks not necessarily having possession of their gold reserves, would be the consequences for the dollar and other western fiat currencies of gold becoming the trade settlement medium throughout Asia, or of the rouble returning to a gold standard. Inevitably, holders of dollars and financial assets, totalling some $30 trillion, would make comparative value judgements not just for the dollar but also for their exposure to other fiat currencies. Not only would this cause private sector actors engaged in cross-border trade to re-evaluate their exposure to fiat currencies as well, but the whole system of fiat currency reserves held by central banks could become threatened.

The strong indications are that Putin supports Glazyev’s thesis. But he has a wider remit, including military strategy over Ukraine. NATO is now committed to the Ukrainian proxy war for as long as it takes. It will require a swift victory by Putin to end this misery, and increasingly the rest of the world knows it. But almost certainly, the forthcoming military escalation by Putin will destabilise financial markets in the western alliance.

A renewed panic in energy and commodity markets seems certain, which will lead to fears in the western alliance’s financial markets of higher price inflation for longer, driving bond yields up and equities lower. Neo-Keynesian investors might initially expect the uncertainty arising from renewed military action to drive global liquidity into the dollar, which is their traditional safe haven, rather than gold. But US-centric markets fail to appreciate that at $30 trillion the currency and financial assets are already over-owned by foreigners, while physical gold is not. And they fail to appreciate that Putin can exploit this weakness.

It would be a good time for Putin to encourage financial conditions to deliver a major blow to the dollar’s hegemony. Under cover of the battlefield, Russia could let markets drive up prices of nearly all her exported commodities. It would then be seen by neutral nations as a market response to the western alliances’ political imperatives. But soaring energy and commodity prices will reflect a sharp decline in the purchasing power of the dollar and its fiat currency cohort of euros, yen, and sterling.

Yet again, by pursuing its military and political objectives in Ukraine, the western alliance would be seen by the wider world to be entirely responsible for collateral financial damage. And that surely, must suit Putin.

Constructing a trade medium of exchange

We now turn to the mechanics of constructing a new trans-national gold-backed currency. One condition which will need to be in place is for a value for gold measured in goods to back inter-Asian trade. Despite the accumulation of gold by the central banks of the Shanghai Cooperation Organisation membership, some of them may not have sufficient official gold reserves to cover their balance of payments deficits except for limited times, requiring a higher gold value in order to do so. And other members, such as Russia, could see continual accumulation of physical gold because of her balance of payments surplus. Ideally therefore, instead of trade settlements being entirely in physical gold, they should be facilitated by a banking system whose credit values are securely based on gold to ensure flexibility.

The task therefore is to design an entirely new non-national currency backed by gold, specifically created for cross-border trade and commodity transactions. Presumably, this is what Glazyev is trying to achieve instead of the more cumbersome EAEU project originally announced. It is a relatively simple task and does not require blockchains and the paraphernalia of a CBDC. The mantra should be to keep it simple, and therefore have no mystery.

The bulleted list that follows is a brief outline of how a new trade settlement currency based on gold can be established to replace the fiat dollar in all transactions between SCO/BRICS member nations. By being completely independent of national currencies, it should be politically acceptable to all involved, as well as a long-term practical solution to facilitate the Russian-Chinese axis’s ambitions for an Asian industrial revolution, free from interference by America and her allies.

The essential elements are as follows:

The announcement of the creation of a new central bank (NCB) and a new gold-based currency on the lines below will be made in advance of implementation to allow bullion markets to adjust to the new regime before it comes into existence.

A new central bank is then established, whose function is to issue a new book-entry currency backed by physical gold, issued and available only to participating central banks. It will be designed to be a fully trusted gold substitute, independent from fiat currency values.

The new currency will only be redeemable for physical gold by participating central banks. They will also be free to add to their NCB currency reserves by submitting additional gold to the NCB at any time.

The NCB’s eligible participants will only be the central banks of participating nations, limited to member nations of the SCO, EAEU, and BRICS. The NCB’s currency is issued to the national central banks against their assigning a minimum 40% gold backing for it. For example, currency representing one million gold grammes secures an allocation of 2,500,000 currency units denominated in gold grammes. The gold does not have to be delivered to a central storage point but can be earmarked[iii] from within a participating central bank’s gold reserves, on condition that they are securely stored in vaults on a list approved by the NCB.

Commercial banks trading in member nations and elsewhere will be free to create and deal in credit denominated in the NCB’s new currency. Issuers and users of this credit are always free to acquire physical gold in the markets, should they wish to back credit created in the new currency with gold itself.

All taxes and restrictions on gold ownership must be fully removed by participating nations. Gold’s legal status as money must be reaffirmed, if necessary.

An efficient central clearing system for commercial banks dealing in credit based on the new currency will need to be established.

Accompanied by the major energy producers setting price benchmarks, commodity exchanges in member nations will be required to price all products in the new NCB currency, replacing pricing in US dollars completely for trade between participating member nations. They can still quote prices in dollars for others should they so wish.

The purpose of the new currency is to provide the basis for trade finance and other cross border financial settlements on a sound money basis. It is also likely to lead to participating nations placing a greater emphasis on their own currencies’ stability while providing a safe haven from a fiat currency systemic collapse.

All empirical evidence informs us that when gold becomes the means by which credit is valued, credit’s own value is not dependent on stability in the quantity of credit, taking its value from gold. This stability imparts pricing certainty to trade and investment, necessary conditions for maximising economic progress particularly in the context of wider industrial development throughout Asia.

Constructed on the lines above, remarkably little physical gold would be required to underwrite cross-border payment values for trade in Asia and beyond. This trade settlement currency should be simple and quick to establish. It must be free from interference from members of the western alliance trying to preserve their own fiat currency systems. And the 40% gold backing rhymes with the basic requirement for a metallic monetary standard set by Sir Isaac Newton, when he was Master of the Royal Mint.

For participating central banks, the replacement of gold in their reserves for allocations of the new currency would represent a significant increase in their reserves. As confidence in the scheme builds, it could be argued that only minimal gold reserves need to be retained by participating central banks, with the balance swapped for the new currency. For example, the Reserve Bank of India officially possesses 795 tonnes of gold. Converted into the new gold currency, its value in reserves is uplifted to 1,988 tonnes equivalent.

ENB Top NewsENBEnergy DashboardENB PodcastENB Substack

Energy News Beat