Examining the energy markets today, we must consider the tariff war currently underway between the United States and the rest of the world. Make no mistake, this is a rightsizing of tariffs, and people are losing sight of the word “reciprocal.”

The factors that contribute to China’s role in holding up the exports of critical minerals to the United States have several key elements.

David Blackmon is a true energy leader and brings up some great points, and I enjoy my podcasts with him, learning from his decades of experience. On the critical minerals, he got me thinking about how this will impact the negotiations of the tariff wars.

I’ve received several inquiries from readers since posting the interview I did with NTD News last week related to China’s new restrictions in the export of rare earth minerals to the United States. In that interview, I emphasized the reality that supply of rare earth minerals is not a problem: Enormous supplies of them exist in situ all over the world, including in the United States, which has abundant known reserves.

The excellent illustration atop this piece shows the known deposits of rare earth minerals globally.

But the US government makes the permitting of mines to produce these known reserves virtually impossible to achieve, meaning we must import them from other countries. Amid our rising cold war with China, the crucial point related to national security here does not relate to the production of these minerals, but to the refining and processing of them.

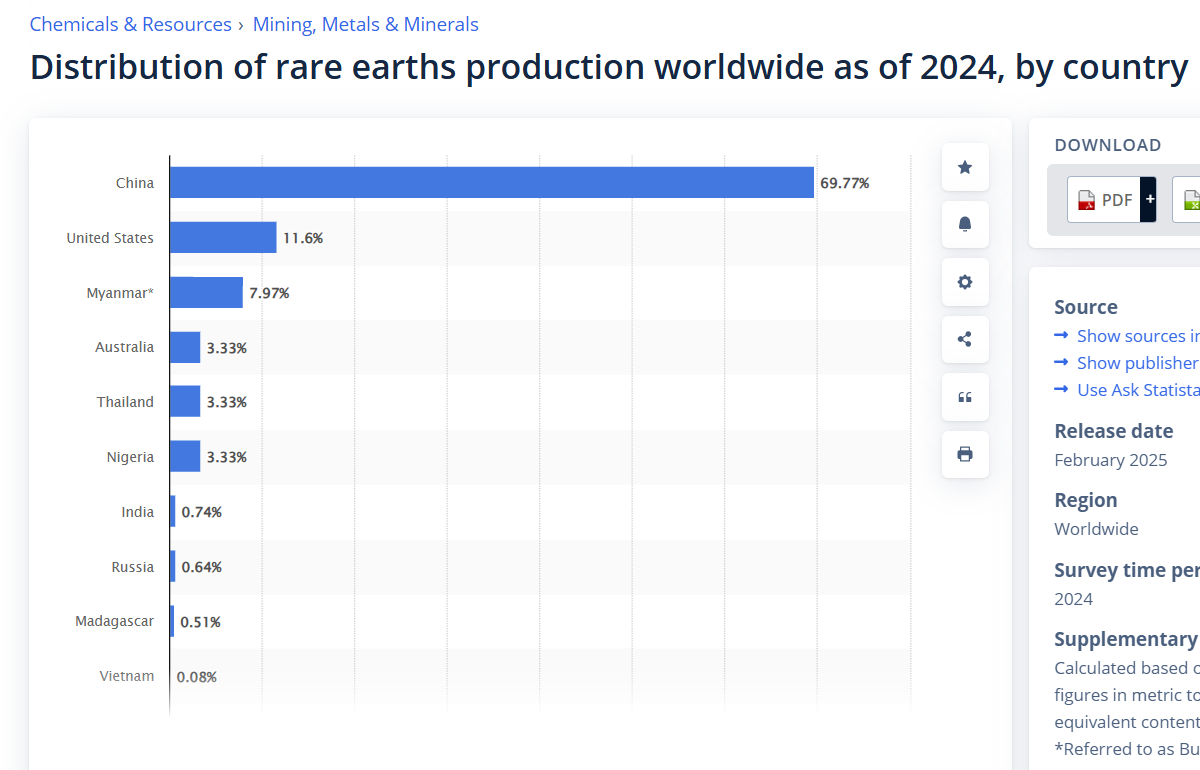

The stark reality is that the U.S. produces less than 12% of global rare earths, while almost 70% are produced in China, as shown in the chart below.

Worse, China controls roughly 90% of global rare earth refining capacity, meaning that regardless of where the minerals are mined and produced, most all of the 30% produced by other nations are loaded onto ships headed for China to be processed. After they are processed, they are then distributed via supply chains under Chinese control.

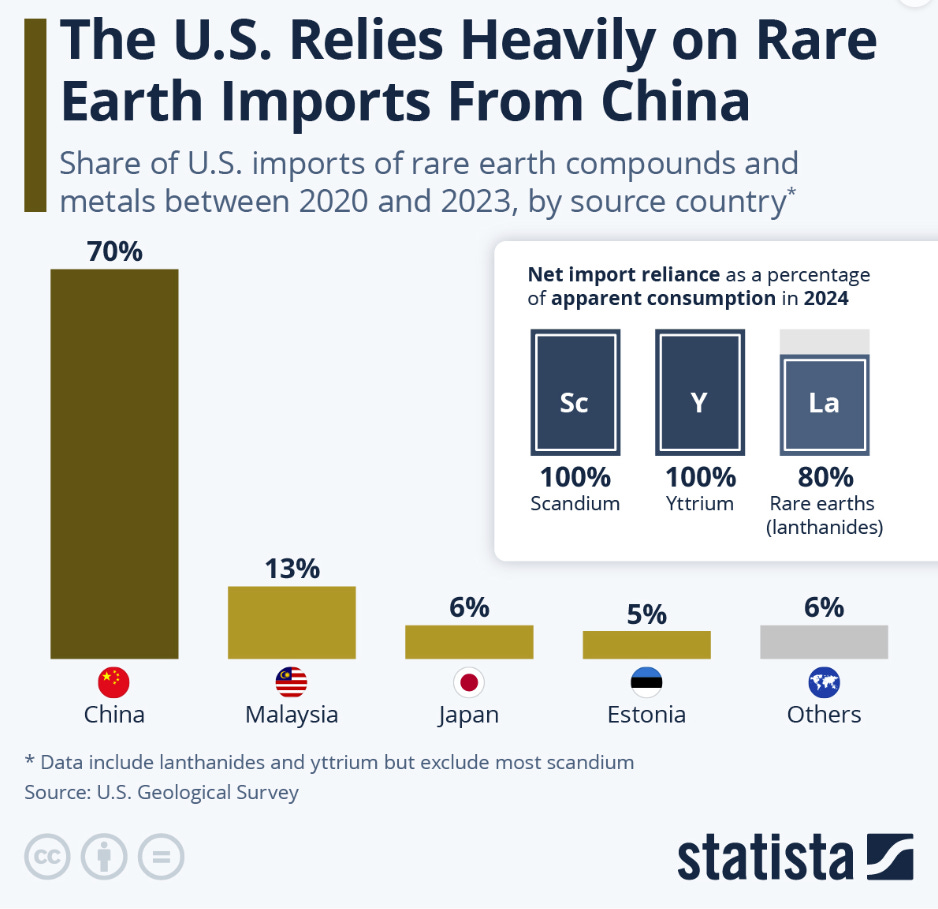

From 2020-2023, per Statista, the U.S. imported 80% of its rare earth needs from other countries. Of those imports, 70% arrived on ships loaded in China:

David is spot on, and we are in a massive time crunch. China has one timeline, and President Trump has another, and both have different fuses.

I started looking into several key issues surrounding critical minerals, and we can transition from zero to full production in 3 to 5 years for gallium. Gallium is used in essential military radar, 5G technology, smartphones, lasers, and integrated circuits. We do not have 3 to 5 years of supply sitting on the shelf, so this puts a new light on the urgency in what we used to call a Mexican Standoff, or a Snow Mexican Standoff, when discussing Canada and their tariffs.

Semiconductors:

Gallium Arsenide (GaAs): Used in high-performance electronics, such as RF chips for 5G smartphones, satellite communications, and military radar systems. GaAs offers superior electron mobility compared to silicon.

Gallium Nitride (GaN): Powers high-frequency, high-power devices like fast chargers, electric vehicle inverters, and 5G base stations due to its efficiency and heat resistance.

Optoelectronics:

LEDs: Gallium-based compounds (e.g., GaN, GaAs) are essential for light-emitting diodes used in displays, lighting, and automotive headlights.

Lasers: GaAs is used in laser diodes for fiber optics, Blu-ray discs, and medical equipment.

Solar Energy:

CIGS Solar Cells: Copper Indium Gallium Selenide cells are used in thin-film solar panels, offering flexibility and efficiency for renewable energy applications.

Alloys and Metallurgy:

Low-Melting Alloys: Gallium’s low melting point (29.76°C) makes it ideal for fusible alloys, liquid metal cooling systems, and thermometers.

Aluminum Enhancement: Gallium improves aluminum alloy properties for aerospace and structural applications.

Medical and Research:

Radiogallium (Gallium-67): Used in nuclear medicine for imaging tumors and infections.

Neutrino Detection: Gallium is used in experiments like GALLEX to detect solar neutrinos.

Quantum Computing: GaAs substrates support quantum dot technologies.

So what will it take for the United States to kick the tires and light the fires to create critical mineral processing centers?

I asked Grok on X what it would take and was impressed with Grok 3.0 and some of the analysis it provided. What we need is speed, money, and regulation cutting or SMRC.

Estimated Timeline

Year 1: Market study, site selection, permits, and partnerships.

Year 2: Plant design, construction, and equipment installation.

Year 3: Pilot operations, process optimization, and initial production.

Year 4+: Full-scale production, assuming stable prices and supply.

Financial and Economic Considerations

Capital Investment:

$50M-$200M for a mid-scale plant, including land, equipment, and initial operations.

Nyrstar’s proposed Tennessee facility is budgeted at $150M.

Operating Costs:

Energy: High due to electrolysis and refining.

Raw Materials: Bauxite/zinc ore prices fluctuate with aluminum/zinc markets.

Waste Management: Acid waste and red mud disposal add costs.

Revenue Potential:

Gallium price: $978.50/kg (April 2025), up 29.47% from 2024.

Demand growth: Driven by 5G, semiconductors, and solar (CIGS cells).

Risk Mitigation:

Price support mechanisms (e.g., US “Resilient Resource Reserve”) to stabilize revenue.

Partnerships with governments or allies (e.g., US-Australia Critical Minerals Compact) for subsidies or contracts.

One key point was the source of the gallium, which could be the coal ash found at coal ash deposit sites all over the country. This would be the most cost-effective approach, as the ash has already undergone partial decomposition, unlike regular mineral ore mining and processing.

As there is only one proposed facility in the United States, owned by Trafigura, exploring a $150 million germanium and gallium recovery and processing facility at its zinc smelter in Tennessee. This project is still in the viability testing phase and not yet operational. Experts estimate that it takes 12-18 months to bring such a plant online once it is approved. So we at least have one in the pipeline. But it will leave us short on the supply side. The defence contractors would be the first ones receiving products.

The proposed Trafigura-owned Nyrstar facility in Clarksville, Tennessee, aims to produce up to 40 metric tons of gallium and 30 metric tons of germanium annually. This output could meet approximately 80% of the U.S. annual demand for these critical minerals, which are extracted as byproducts of zinc smelting.

For context, the U.S. consumed approximately 19,700 metric tons of gallium in 2022. However, earlier data (2016-2020) suggests a much lower average of 16 metric tons annually, indicating potential discrepancies in reporting or a significant demand spike. If the 2022 figure is accurate, the proposed 40 metric tons would cover only a small fraction of total consumption. Still, if the lower historical average holds, it could nearly meet or exceed demand for raw gallium.

Closing Thoughts

This is all speculation, as we are in the middle of the tariff war, and it is unclear who will blink first. I think what will happen is the permanent decoupling of several systems worldwide.

Energy security starts at home, and I genuinely do not understand why the UK’s leadership is building grid interconnects like the Scotland connection or an underwater link to Morocco to supply electricity to the grid. You cannot always control what is outside of your borders. The same thought process should be considered in manufacturing, food supply, and health products. Should we make 100% of everything we need? No, we need to trade and be great trading partners, but we should be able to make 100% of the things that can keep the lights on, food, and health supplies.

Buckle up for the next few months and enjoy the ride. I believe we will come out on the other side more prepared to survive and excel in the next 250 years in the United States. Energy security starts at home, and you need to ask yourself. Can I protect my family and keep them safe in an emergency?

Prepare and do not be asleep at the wheel like the Democrats and Republicans who have been for the last 60 years, selling out our shipbuilding and technical manufacturing to China. We are about to pay the price to bring those jobs and capabilities back home.

Who will be the biggest losers? I believe it will be the name-brand clothing and brands that have relied on cheap Chinese labor, and we are now finding out how much money was going into the pockets of designers and clothing brands.