Prices are still way too high, that’s the problem in the housing market, but they’ve been dropping substantially in some cities.

By Wolf Richter for WOLF STREET.

Oh my, here goes the real estate industry’s dream of a recovery for existing homes. Pending sales – a forward-looking indicator of “closed sales” of existing homes to be reported over the next couple of months – dropped 5.5% in December from November, seasonally adjusted, and were down 5.0% from the already collapsed levels a year ago, according to the National Association of Realtors today.

The Buyers’ Strike continues because prices are too high. Compared to the Decembers in prior years:

- Dec. 2023: -5.0%

- Dec. 2022: -2.8%%

- Dec. 2021: -36.1%

- Dec. 2020: -41.2%

- Dec. 2019: -28.2%.

Pending sales have been relentlessly hobbling along the bottom for over two full years. This is what happens when prices spike by 50% in a couple of years. Now they’re just way too high. These too-high prices have frozen the resale market and crushed the brokerage and mortgage industry, including employment (historic data via YCharts):

Pending sales are based on contract signings and track deals that haven’t closed yet and could still fall apart or get canceled. There has been quite a bit of talk of deals falling apart or getting canceled because buyers cannot afford the homeowner’s insurance, or cannot even get it. This is a particular issue in states where homeowner’s insurance has spiked in recent years. These deals that go nowhere are included in pending sales figures, but are not included in the figures of closed sales.

Pending sales by region. Seasonally adjusted, transactions fell in all regions in December:

- West: -10.3%

- Northeast: -8.1%

- Midwest: -4.9%

- South: -2.7%

What NAR said today about this situation in the West and the Northeast: “Contract activity fell more sharply in the high-priced regions of the Northeast and West, where elevated mortgage rates have appreciably cut affordability.” Ah yes, the too-high prices.

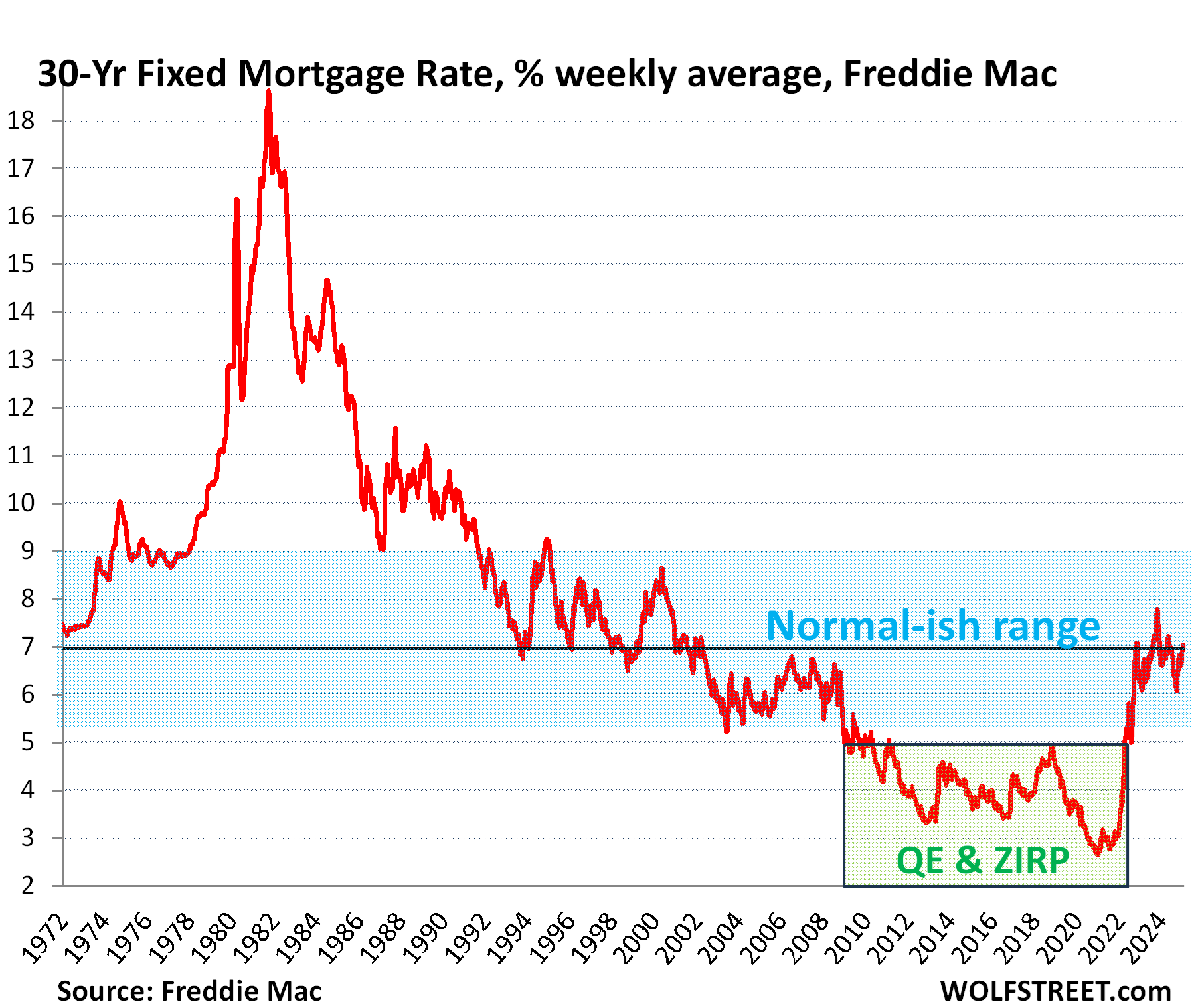

Mortgage rates are back in the old-normal range.

The average 30-year fixed mortgage rate inched down a tad to 6.95% in the latest reporting week, according to Freddie Mac today.

In December, when those pending deals were made, this weekly measure of mortgage rates was between 6.60% and 6.91%, lower than in January.

While those rates are far higher than they had been during the era of the Fed’s interest rate repression and QE, they’re now back roughly in the old normal range before QE.

But the Fed’s QE, which included the purchase of $2.7 trillion in mortgage-backed securities (MBS) to drive down mortgage rates and inflate home prices, ended in early 2022. And in mid-2022, the Fed began shedding those securities, and has so far shed $2.11 trillion. And mortgage rates have sort of re-normalized.

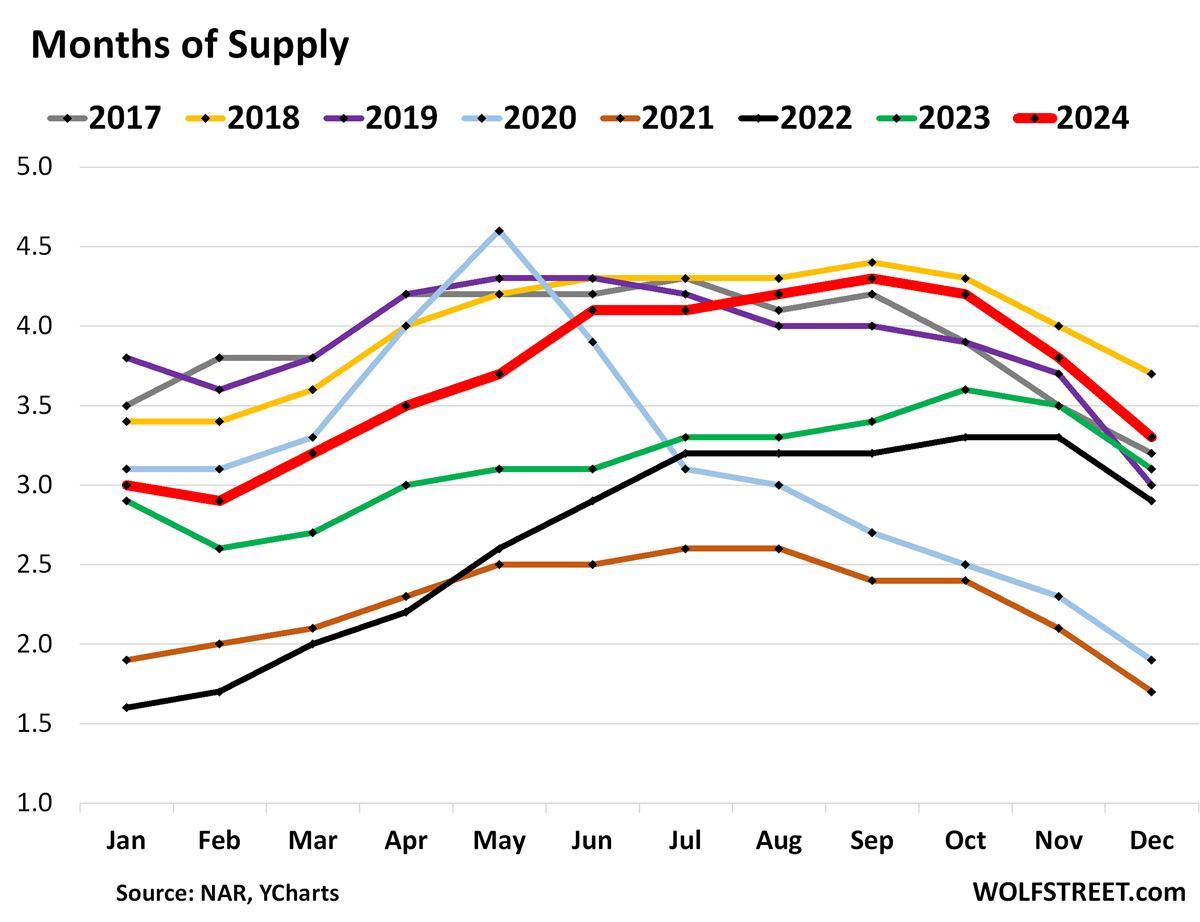

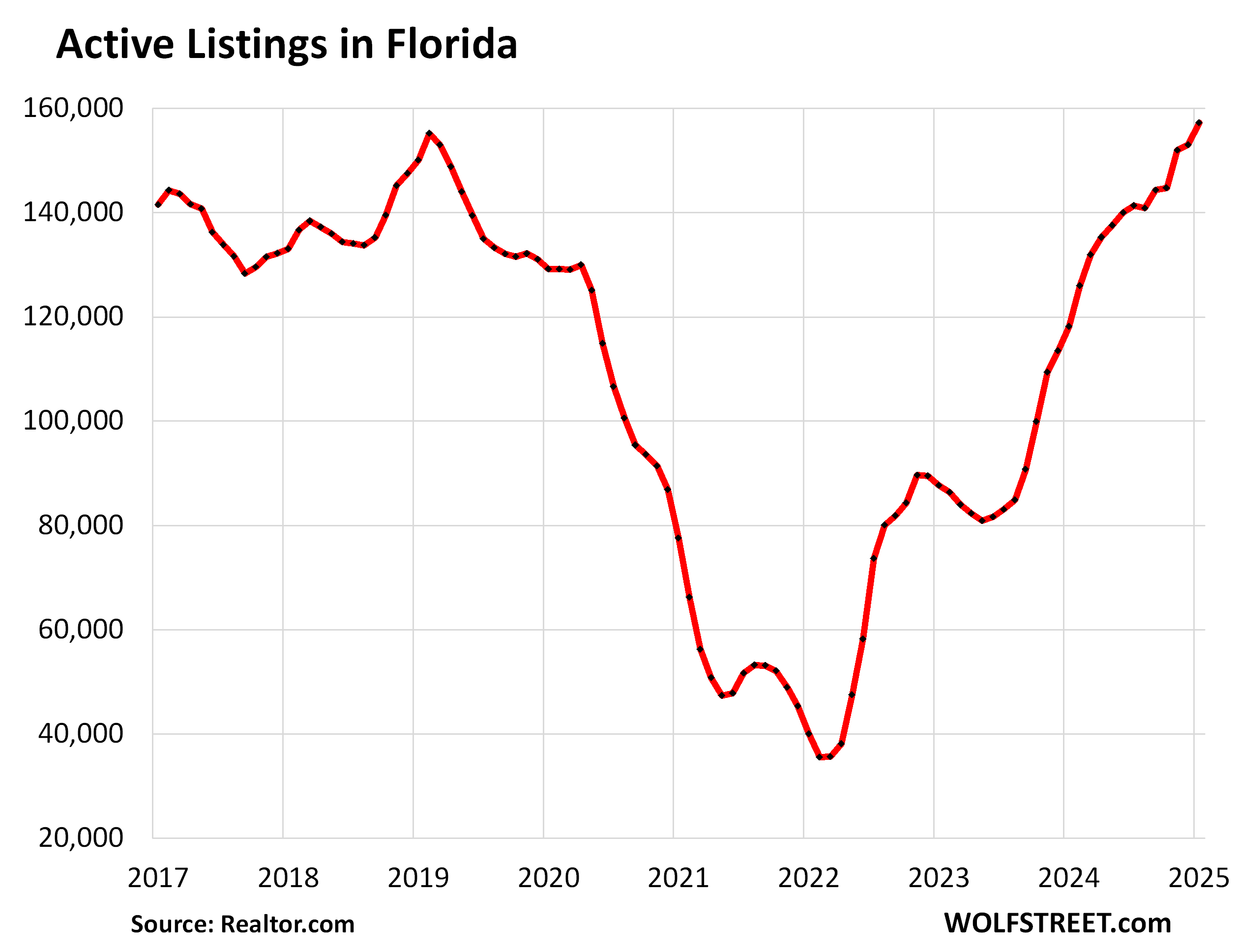

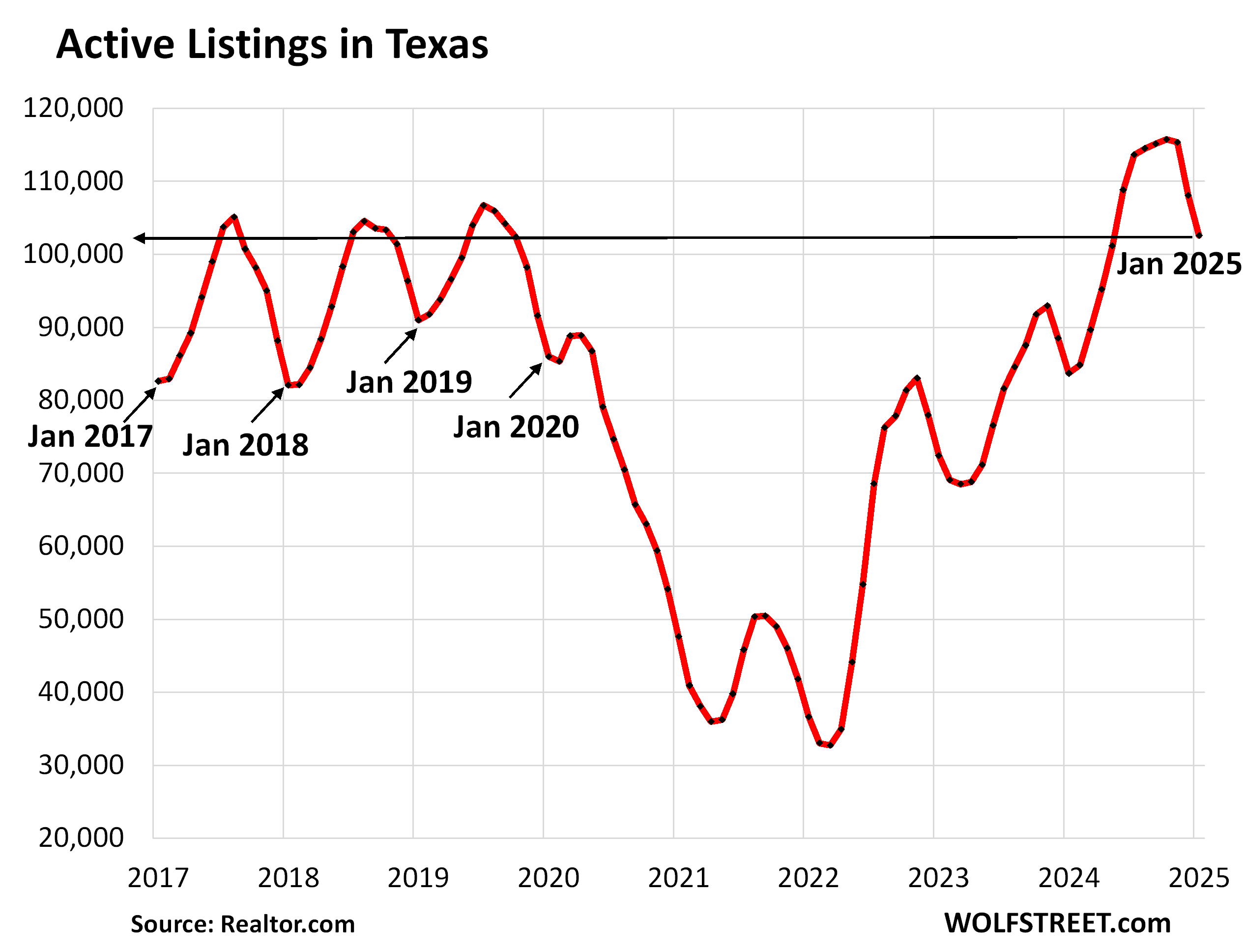

Inventory of existing homes & new construction is piling up, particularly in the South and West.

Supply of existing homes for sale in the US overall, at 3.3 months in December (fat red line in the chart below), was the second highest for any December since 2016, below only 2018, according to NAR data:

In Florida, active listings of existing homes in January ballooned to a record high in today’s data from Realtor.com going back to 2016:

In Texas, active listings of existing homes in January reached the highest level for any January in the data from Realtor.com going back to 2016. Since May 2024, active listing in every month were the highest for that month in the data of Realtor.com (fat red line):

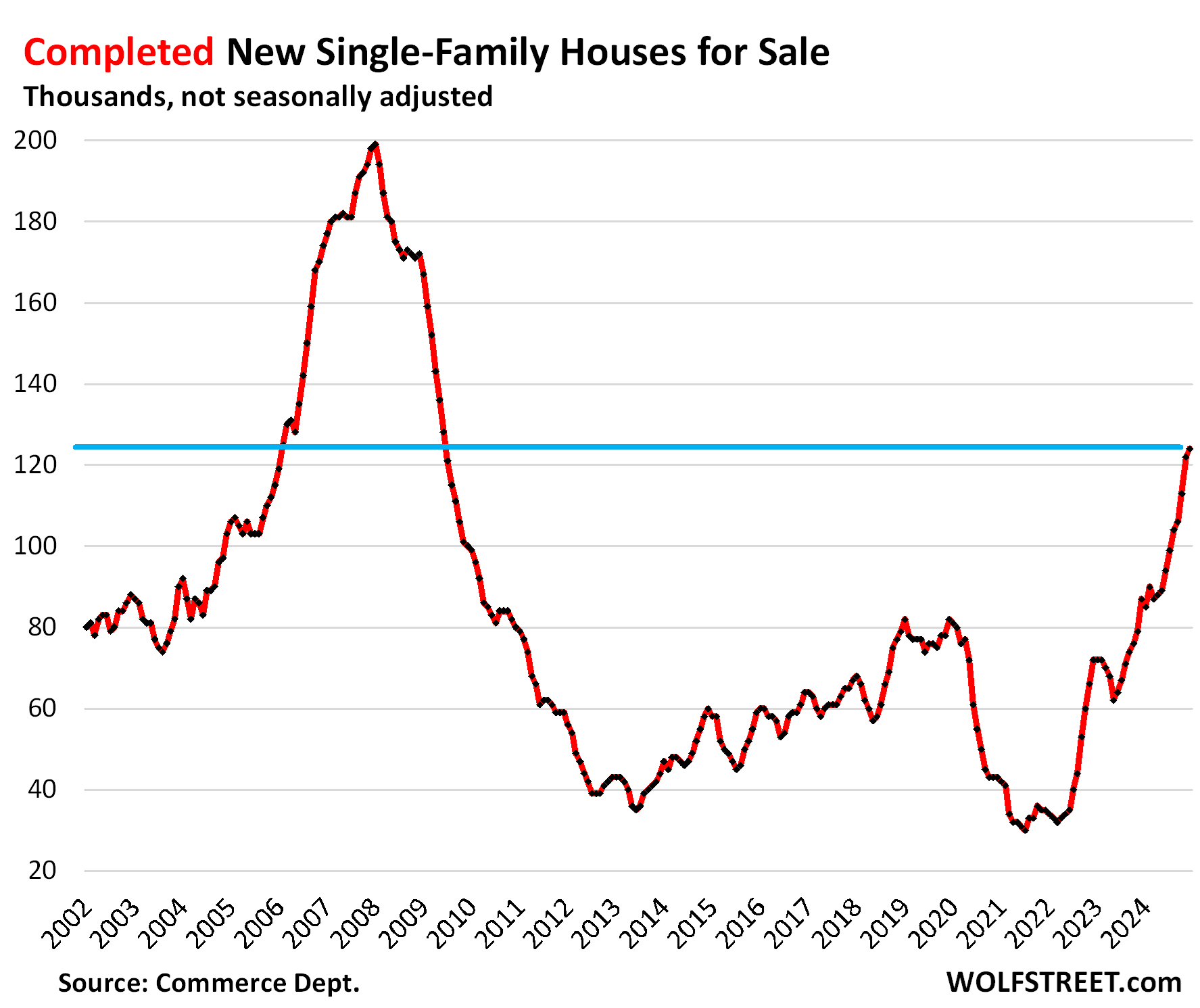

In the US, inventory of completed new houses for sale has spiked by about 50% from the peaks of 2018 and 2019, and by nearly 50% year-over-year to the highest since June 2009, according to Census Bureau data, as we have discussed a couple of days ago:

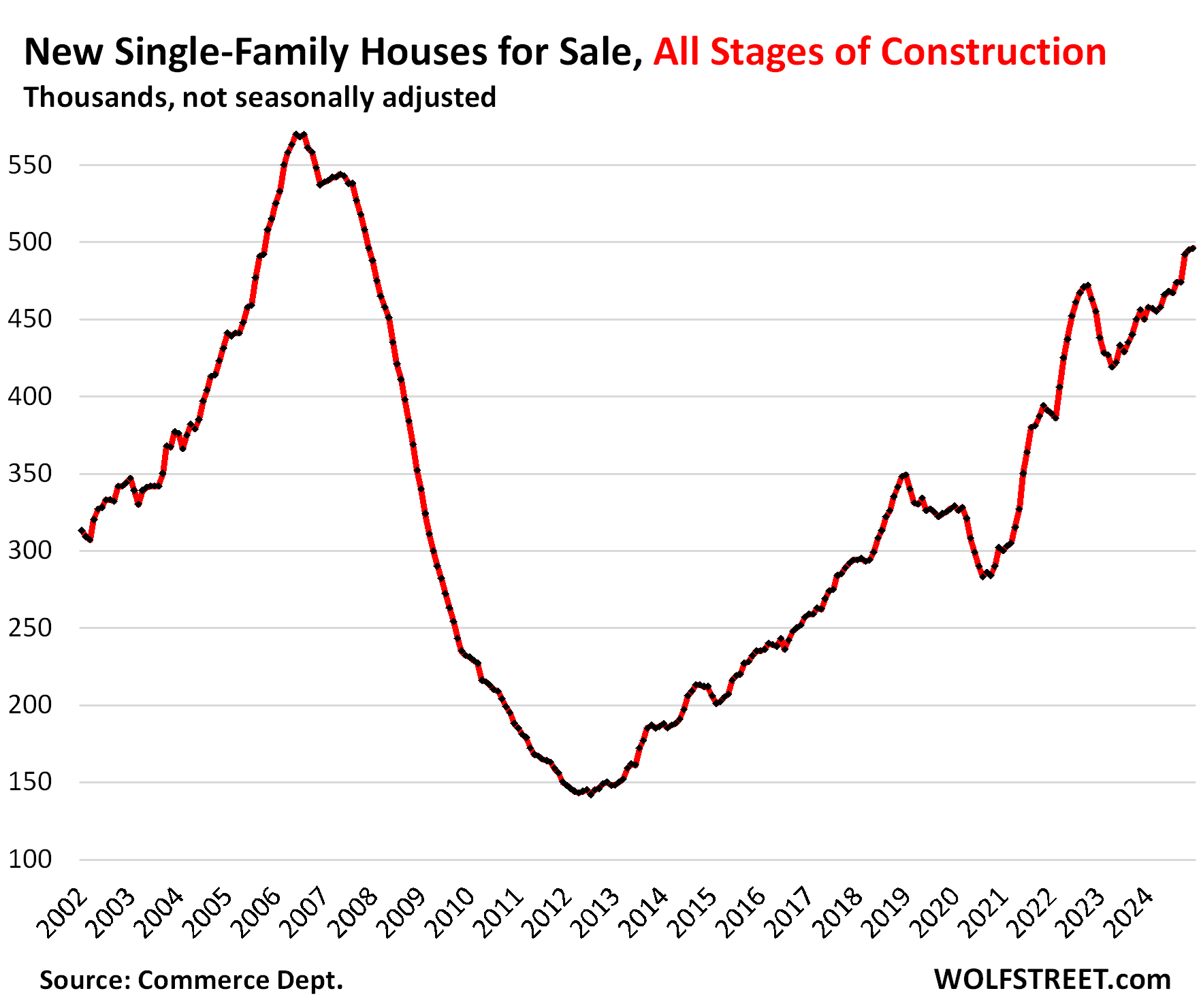

In the US, inventory for sale of new houses at all stages of construction – from not yet started to completed – has ballooned to the highest since December 2007.

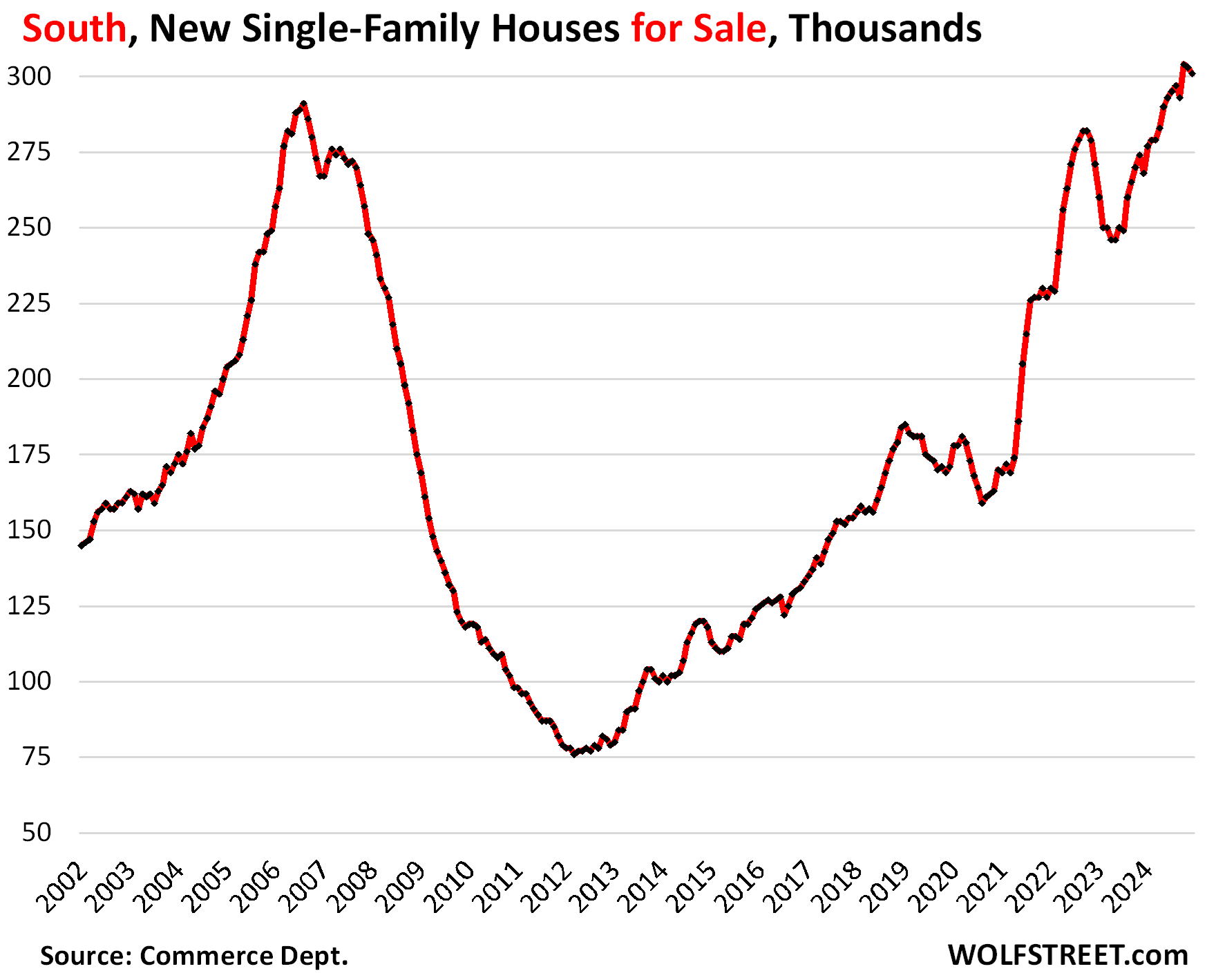

In the South, inventory for sale of new houses at all stages of construction has ballooned past the records during the Housing Bust:

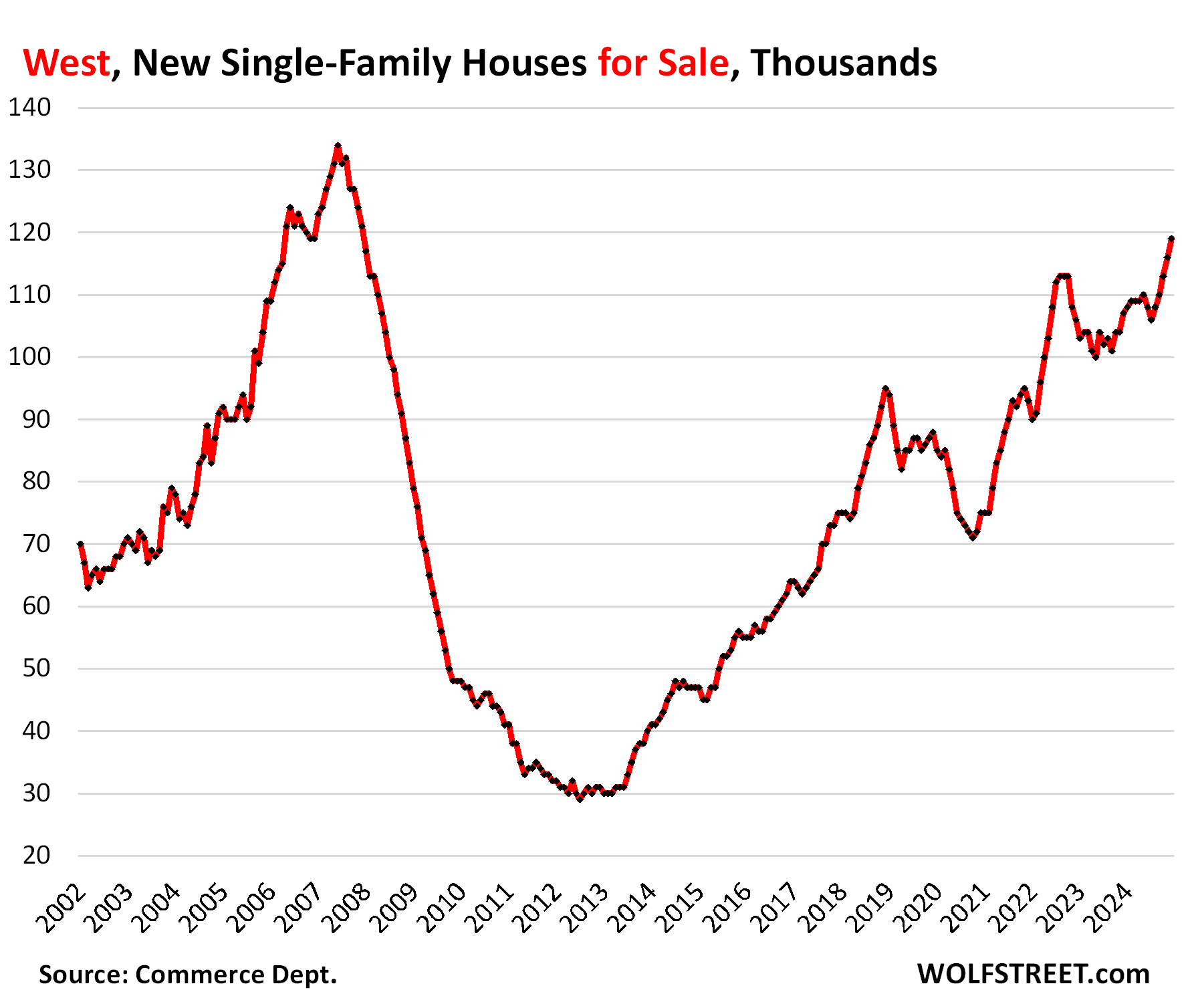

In the West, inventory for sale of new houses at all stages of construction is getting close to the highs of the Housing Bust:

Buyers’ Strike continued because prices are too high.

Pending sales of existing homes, as we’ve seen above, are wobbling along near the bottom, and did so again in December.

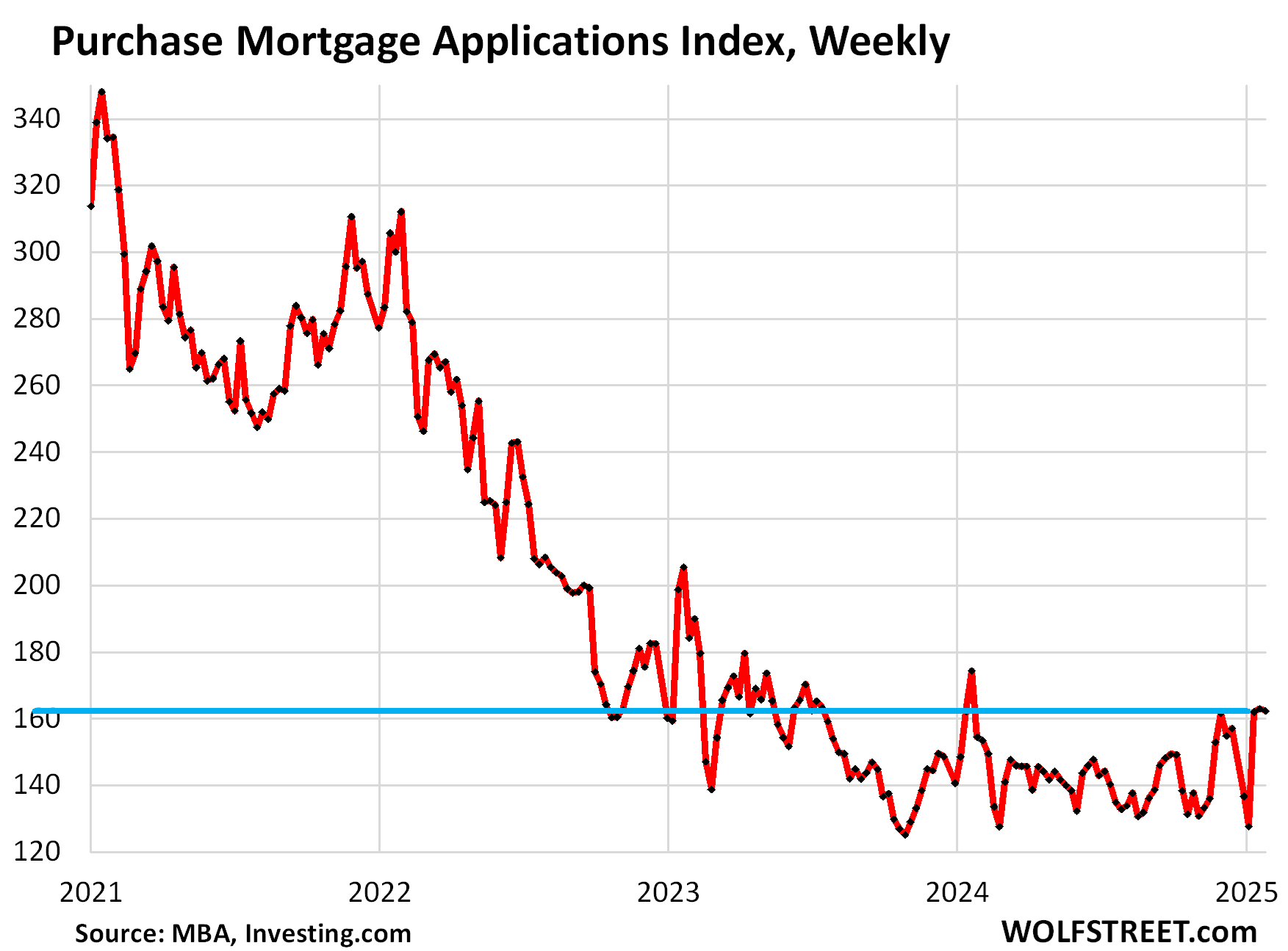

Applications for mortgages to purchase a home, after closing in on the prior lows in November, ticked up a little in December, seasonally adjusted, and in January stayed there, still down by 48% from January 2019 and from January 2021, according to the weekly index of purchase mortgage applications from the Mortgage Bankers Association.

Mortgage applications are an early indication of home sales: like pending sales, up only a smidgen from rock bottom:

Prices have started to decline in many cities. But in some cities – we only track the biggest cities here – prices of single-family houses and/or condos have come down from 9% to over 20%, dropping to levels first seen years ago, for example, in Austin, Oakland, New Orleans, San Francisco, Washington D.C., New York City, Detroit, Seattle, Portland, Tampa, depicted in lots of charts: The Big Cities with the Biggest Price Declines of Single-Family Houses or Condos from their Peaks: From -9% to -21%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Energy News Beat