Thesis

Euronav (NYSE:EURN) is a Belgian oil tanker company which is considered by many as the best-managed, with a strong balance sheet.

Euronav has in 2022 become the object of a merger deal with Norway’s Frontline (FRO), owned by John Fredriksen. The Belgian Saverys family, a Belgian shipping family with strong historical ties to Euronav, has opposed the merger and has raised its stake in Euronav up to 25%, allowing the merger deal to be stopped. Frontline had at first lowered its stake in Euronav, then subsequently raised it to 25% as well.

Euronav’s stock price tanked after Frontline announced the termination of the merger deal. Euronav, however, opposed to that termination and initiated fast-track arbitration proceedings, in light of among others the contractual stipulation that moves of the Saverys family could not be a reason for termination. The request for intermediate measures in arbitration proceedings should apparently have an outcome on February 7, 2023. Though Euronav stands a good chance of having Frontline eventually comply with the terms of the merger deal, nothing is ever certain in court.

I am inclined to think that, though a full merger deal is probably off the table, Euronav stands a reasonable chance to be awarded damages in the case as to the merits, even if a judgment on that may be a year or more away. At the same time, what will come out of the intermediary proceedings is highly uncertain. I see parties settling at a given time.

The tanker market is doing well these days, although the recent EU bans on crude oil had analysts expect higher rates since November. That expectation turned out wrong. Though the winter season is traditionally strong for tanker rates, it is expected that rates remain high for the rest of 2023 at least. There is even talk of an oil tanker super cycle.

The recent merger debacle has made it so that Euronav’s stock did not perform as well as that of peers.

Euronav will report last quarter’s results on February 2, 2023, and has a dividend policy of 80% of its net income. I expect earnings to be strong compared to previous quarters, perhaps even compared to the market given the quality of Euronav’s vessels and overall worldwide fleet utilization.

The tanker order book remains at all-time lows and worldwide fleet utilization is high, allowing the typically volatile prices to remain elevated over a longer period of time.

The Frontline merger

Euronav is a Belgian oil tanker company managed by Hugo De Stoop. It historically related to the Belgian shipping family Saverys, itself owner of Compagnie Maritime belge or CMB, and Exmar (OTCPK:EXMRF).

Frontline is a Norwegian oil tanker company owned by John Fredriksen, a Norwegian industrial magnate.

In an all-stock deal, both companies had announced on July 11, 2022, that they would merge. The merger was supposed to be concluded by the end of 2022, and parties were not allowed under the merger deal to pay out dividends. The merged company would be called Frontline, would relocate to Cyprus, and Euronav’s Hugo De Stoop who is generally regarded as a strong manager who has taken Euronav from a mediocre performer to an outstanding oil tanker company, would become CEO. Together, both companies would form the largest oil tanker company in the world. The merger deal would see rather limited upside for shareholders of Euronav, as explained by Seeking Alpha contributor Bram De Haas.

The Saverys opposition

Over the past months, the Saverys family has strongly opposed the merger deal, considering that Euronav should remain Belgian, and that the merger deal may damage the green intentions the Saverys family had with the company. The Saverys family has raised its stake to a 25% shareholder position, which allows them to block the merger deal.

The Frontline termination and ensuing arbitration proceedings

At that point, Frontline’s John Fredriksen had in first instance lowered his stake in Euronav. Frontline had announced the termination of the merger deal.

Euronav had subsequently stated on January 11, 2023, that it rejected Frontline’s right to terminate the agreement, and has on January 18, 2023 announced that it had started fast-track arbitration proceedings for urgent and interim conservatory measures, requesting the suspension of such termination pending a determination on the merits pursuing primarily the specific performance of the combination agreement.

The merger deal in fact did not allow Frontline to walk away from the deal because of moves of CMB, as appears to result from article 12.6 of the merger deal.

Article 12.6 merger deal (Belgian economic gazette De Tijd)

The fast-track arbitration proceedings will lead to a judgment on February 7, 2023. A request for arbitration proceedings on the merits has meanwhile also been filed by Euronav, as announced on January 30, 2023.

On January 26, 2023, it appeared from a SEC filing that John Fredriksen had now acquired 25% voting power in Euronav through different entities.

Under Belgian corporate law, both the Saverys family and John Fredriksen now have acquired stakes in Euronav that allow them to have a blocking vote, meaning the plans any of both have with Euronav may not go through in the end. They will have to find a compromise at a given point, unless one of them backs out and lowers their stake.

I consider the latter as a real possibility, as Euronav is about to report about $1 billion in earnings, with the oil tanker market expected to remain strong throughout 2023 and possibly beyond. In that case, it is plausible that both either Fredriksen or Saverys, or both, take profits and lower their stakes, and bury the hatchet. The Saverys family does seem to have every intention to do whatever it takes to keep Euronav Belgian. Given Belgium’s tax policy and in light of almost all competitors being located in tax havens, that may make Euronav less competitive compared to its peers. Except for recently in light of recent events and the Saverys family speaking out, Euronav and Hugo De Stoop have not received the appreciation they should have received in Belgium.

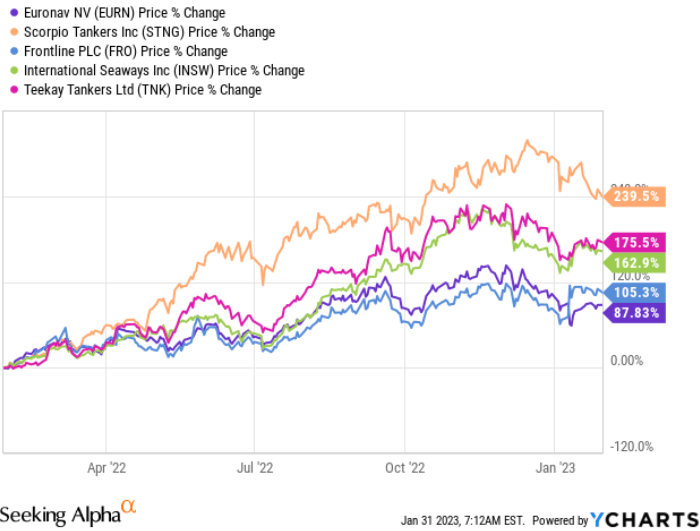

Euronav’s stock price evolution in comparison with peers

Euronav is currently valued at about $3 billion. Along with all oil tanker companies, its share price has considerably risen over the past year. The below chart sets out the rise in several of these well-known companies over the past year on a percentage basis.

Stock chart evolution EURN, STNG, FRO, INSW, TNK (Ycharts)

{kind=link}

One sees Euronav’s stock price move has been fairly low compared to some others, as well as Frontline’s.

The rise in these share prices generally follows the earnings these companies are estimated to make. The best way to do so, in my eyes, is to follow oil tanker spot prices relevant to each of these companies. Each of these companies has different vessels in its float, which requires the comparison to be made on an individual basis. For Euronav, the fleet consists of the largest vessels out there, VLCC’s and Suezmaxes. Furthermore, Euronav has a history of long-term contracts, which makes the spot price estimate fallible. Finally, Euronav’s fleet is one of the newest, which generally allows the company to charge higher rates in comparison to other vessels. In that sense, earnings are important, and analysts can only guess how well – or not – a company has done over a past quarter.

Quarterly results and further oil tanker rate guidance

Euronav will announce quarterly results on February 2, 2023. Euronav is expected to post quarterly earnings of $1.01 per share, representing a change of +365.8% year-over-year, with revenues expected to be $362.95 million or 325.3% compared to a year ago.

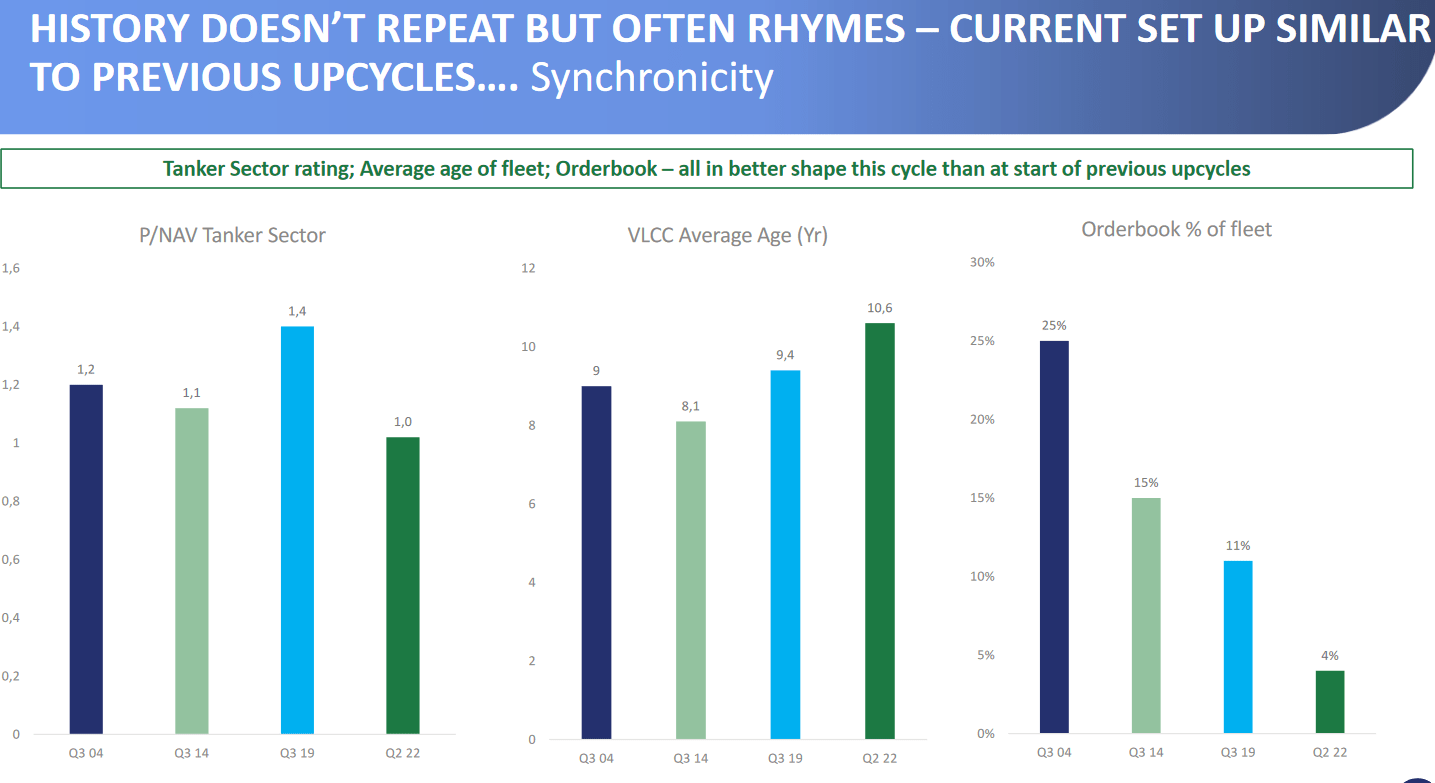

That abrupt change correlates to a highly price-volatile oil tanker market, in which the fleet is old and the order book for newbuilds is historically low. Given the time it takes to build these vessels, the fleet is unlikely to expand in the coming years, and possibly reduce.

Optimistic oil tanker market dynamics (Q3 earnings presentation)

{kind=link}

Euronav gave the following guidance during the latest quarterly call:

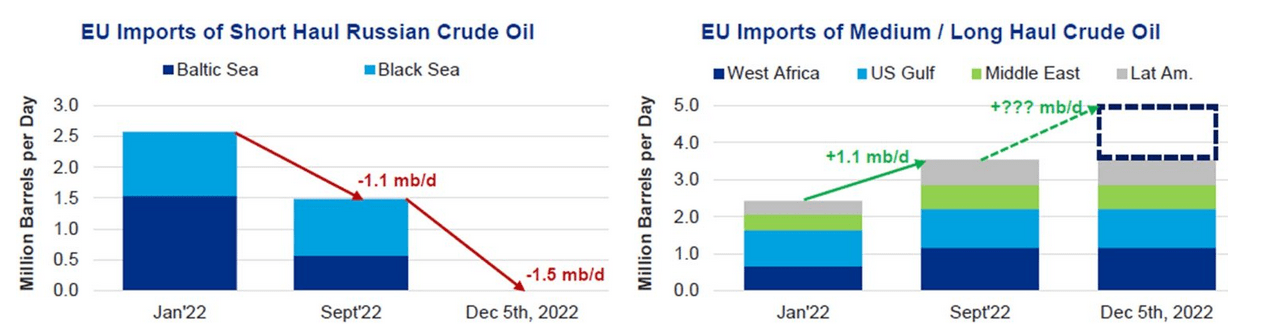

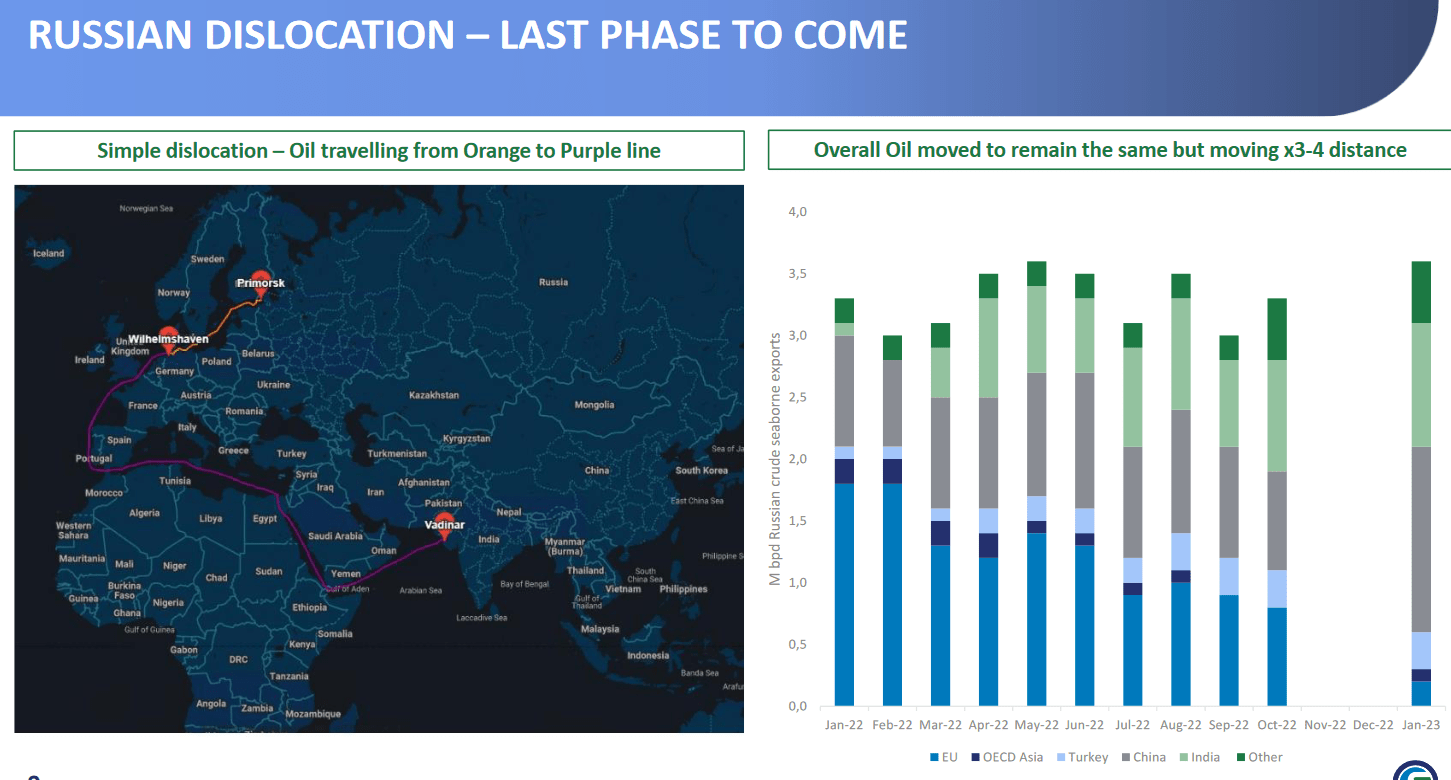

The European Union has already diverted about one million barrels per day of seaborne imports from Russia and replaced those largely from Atlantic and the Middle East locations. We expect another one million barrels per day, of the EU bound exports from Russia to follow a similar pattern over the next quarter, ahead of the fifth of December deadline set without EU to ban oil, all oil shipped from Russia to Europe. This will mean that the sale in world would travel, approximately three to four times the distance it previously did. We will continue to see the benefit of substitution trades from Atlantic to Middle East, oil being taken on a seaborne route to the EU. This latter substitution trade, will in particular benefit the larger custom sizes such with the VLCCs. This trend has been very pronounced since July onwards.

It is that dynamic, together with other factors such as an EU ban on Russian oil, longer trade routes, a possible reduced fleet, a reopening world including China and preference for oil compared to relatively higher-priced gas, that has some analysts raving about times to come.

Revised oil tanker traffic routes (Freightwaves)

Rerouted longer routes (Q3 presentation Euronav)

{kind=link}

{kind=link}

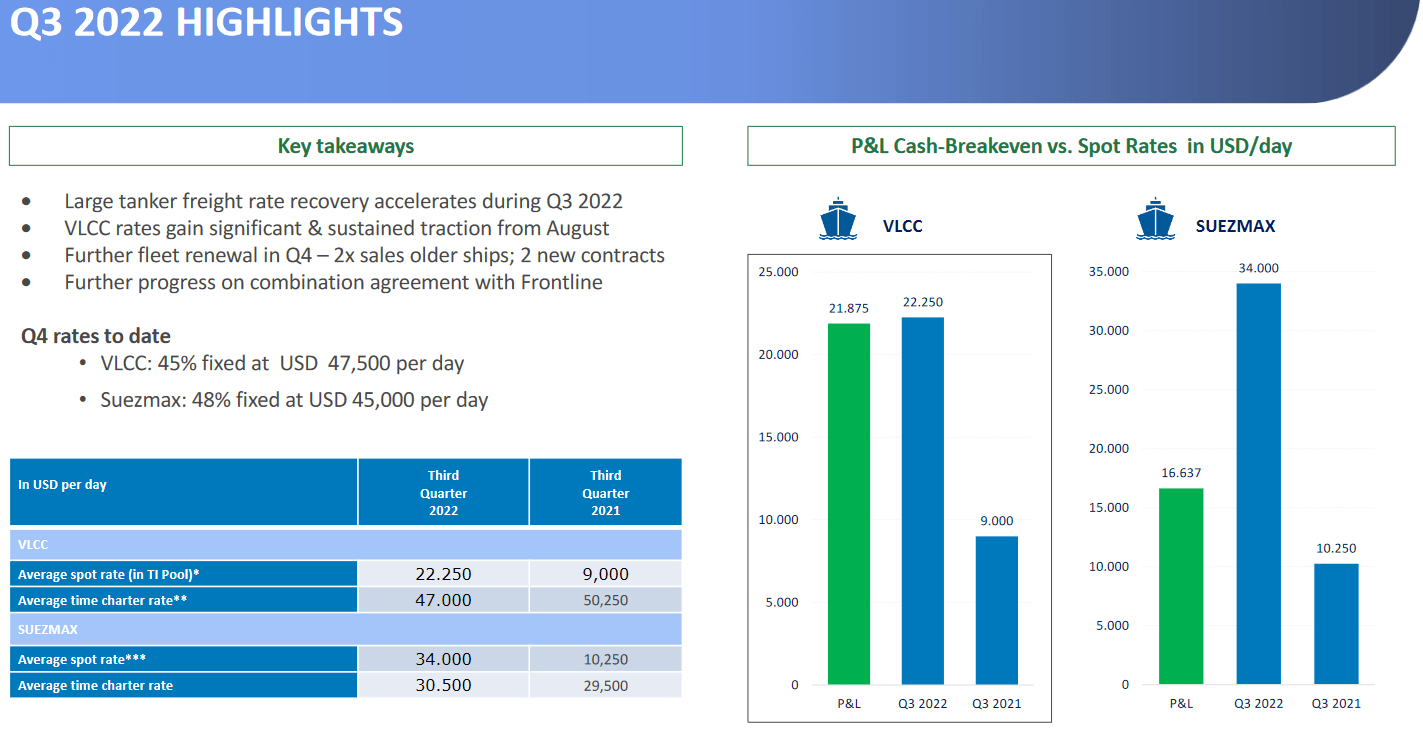

For the last quarterly results, Euronav gave guidance that VLCC has gained significantly with sustained traction, with spot rates for the fourth quarter of 2022 already 45% fixed at 47,500USD per day for VLCC, and 48% fixed at 45,000USD per day for Suezmax vessels. In comparison, for the third quarter, guidance was that date spot rates were 47% fixed at $12,700 per day VLCC and 49% fixed at $23,900 per day Suezmax.

With a standard VLCC being profitable at around $25,000 per day, Euronav making reference to a lower break-even rate, and the company generally profiting from good prices for its newer and more environmentally-friendly vessels, the future may be bright.

Q3 Euronav highlights (Q3 presentation)

{kind=link}

In coverage of January 15, 2023, Seeking Alpha contributor True Orion explained well, for DHT Holdings (DHT), how one-year VLCC contracts are valued at $37,500 per day, and that industry experts believe the strong market dynamics will continue through 2023 and possibly beyond.

The oil tanker market remains hard to predict. Clarkson’s did expect the ban on Russian oil to see VLCC spot rates going up to $150,000 per day, but that never happened. Instead, the EU ban led to plummeting VLCC rates.

Still, renowned fund manager Joakim Hannisdahl had on October 13, 2022, considered that the market could see a so-called super cycle. Mr. Hannisdahl is well-respected in the industry, and had been ranked #1 shipping analyst globally by Bloomberg for a number of years.

J. Hannisdahl tweet re. super cycle (Twitter Joakim Hannisdahl)

For the first weeks of 2023, VLCC spot rates were $49,000 per day reported the first week, and around $37,000 to $39,000 the weeks after.

Dividend policy

Euronav has a dividend policy targeting a return of 80% of net income to shareholders, primarily in the form of a cash dividend, before taxes.

The question is, how this dividend policy is to be affected, now that Frontline terminated the merger deal, and Euronav has disputed it. If Euronav considers the termination unlawful, it could take the position that the merger deal is still applicable, and that it cannot proceed to pay dividends. Possibly the interim decision in arbitration proceedings may bring clarity in that regard, though that would touch upon the merits of the case.

This was Euronav’s guidance in the last quarter:

Yes absolutely. I mean when you do a merger and you calculate the economics namely the ratio, you are normally freezing the dividends. So otherwise, the economics are changing. So what we have in the agreement is obviously, we can continue to pay a minimum dividend the €0.03 that we pay every quarter that’s in the books. But we are now moving to a market that should allow us to return more capital to the shareholders. And we will do so but only after we have the tender over – the tender offer closed and that’s obviously the same for frontline and they have paid a dividend in Q2 that was also agreed and calculated in the ratio.

But then we should hold on paying dividends until the tender offer is closed and that we expect as you’ve seen to be on in Q1. So there might be a little lag of a quarter and even not a full quarter, I mean probably one or two months, if you look at your calendar and when we pay dividends related to every quarter.

We may find out on February 2, 2023, how Euronav now looks at this.

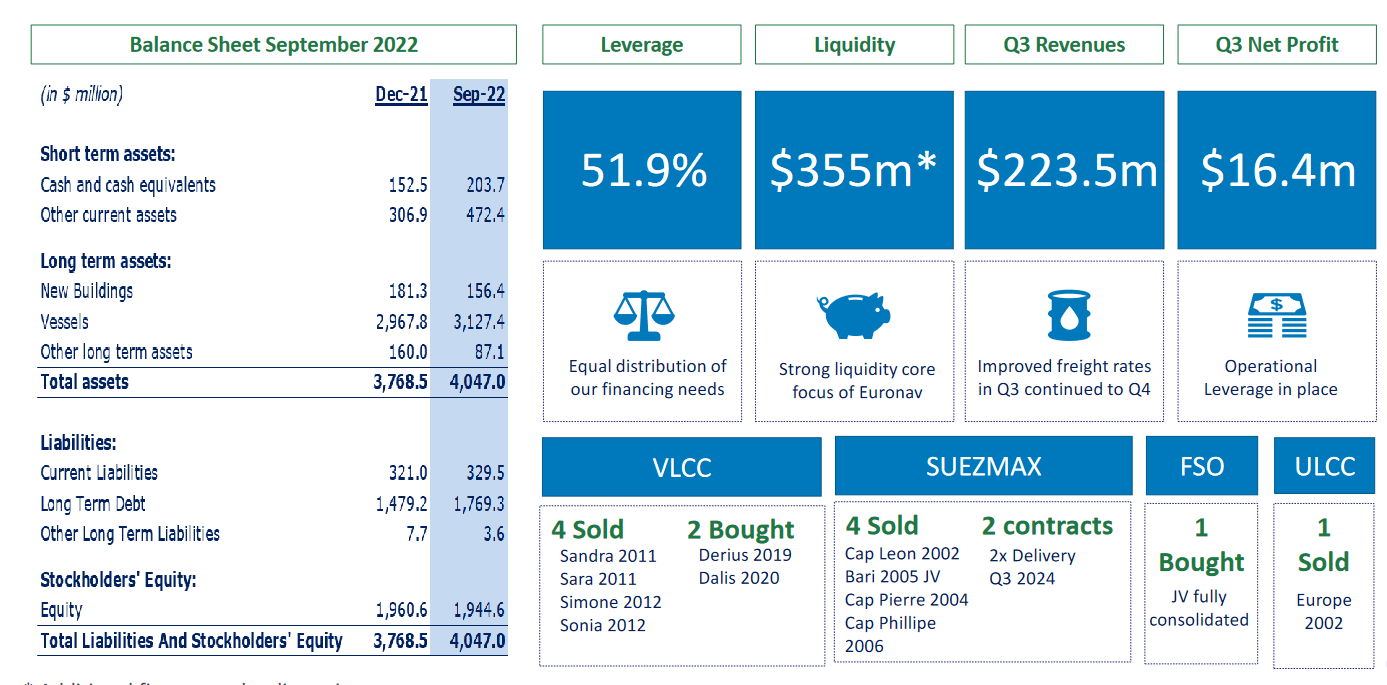

Meanwhile, Euronav has strong financials and $800 million of liquidity as reported in the last quarter.

Financials sheet (Q3 report presentation)

{kind=link}

Conclusion

The saga between Euronav and Frontline with regards to their merger deal, as announced in July 2022, has not yet come to an end. An intermediary judgment is expected by February 7, 2023.

The Saverys family on the one hand and John Fredriksen have their guns drawn. By increasing their positions in Euronav, both seem to have profited from the good oil tanker economics, and the pullback in Euronav shares after the merger deal tanked.

Euronav is expected to report good earnings, though some had expected them to be even more profitable. The company is expected to report $362.95 million in revenue.

Guidance for the sector is that the oil tanker market will remain strong for the rest of 2023, and possibly longer. Some have even mentioned the word ‘super cycle’.

What will happen with the announced dividend payout of 80% of net income, next to a fixed €0.03 payout, is unclear at this time. I expect Euronav to address this in the quarterly call.

ENB Top NewsENBEnergy DashboardENB PodcastENB Substack

Energy News Beat