Lennar shocked the market by saying it’ll address this situation with further price cuts; its average price to drop by 16% from the peak in 2022.

By Wolf Richter for WOLF STREET.

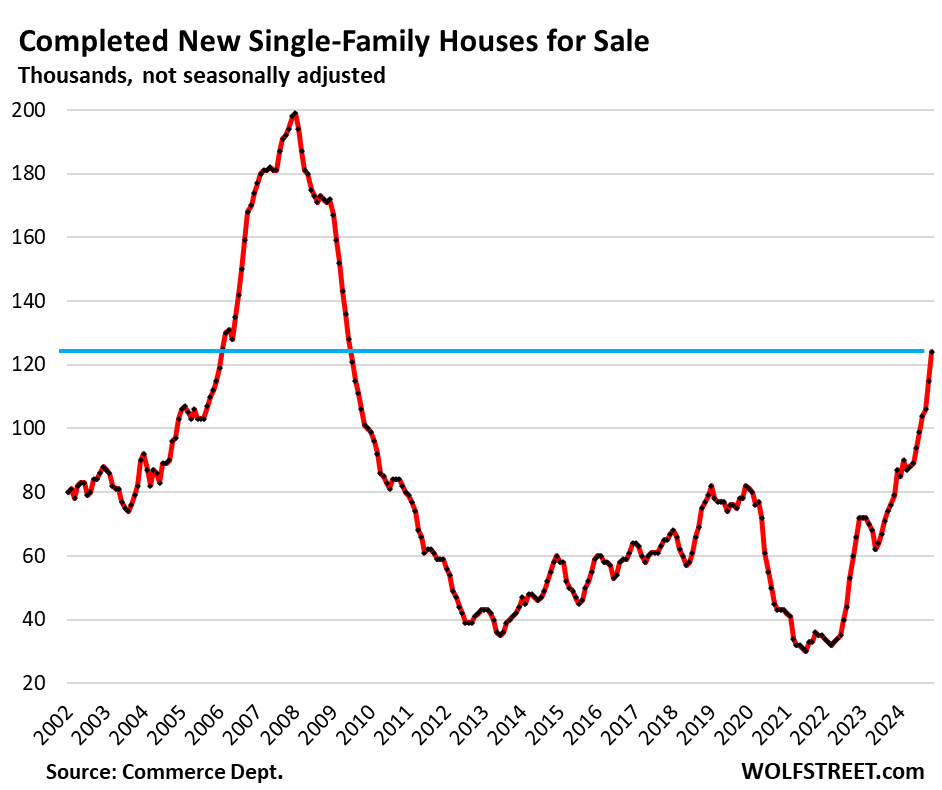

Unsold inventory for sale of completed new houses spiked by 57% year-over-year to 124,000 houses in November, according to Census Bureau data today, the highest since June 2009 during the depth of the Housing Bust when homebuilders, stuck with a huge pile of completed houses amid plunging demand, were trying to survive.

Homebuilders are trying to find buyers for these completed “spec” houses by piling on incentives, including costly mortgage-rate buydowns, and by cutting prices. But obviously, they haven’t done nearly enough to trim their bloated inventories, which continue to balloon, and they’ll have to do a lot more to bring those prices and payments down.

This surge of completed, essentially move-in ready supply is good news for the overall housing market, though not for homebuilders, and not for homeowners that want to sell an existing property. These “spec houses” will need to be sold quickly because builders have sunk a lot of capital into them, and because builders are continuing to build at a faster clip than they’re selling them – though they’re selling them at a pretty good clip – thereby adding to the pile on a monthly basis.

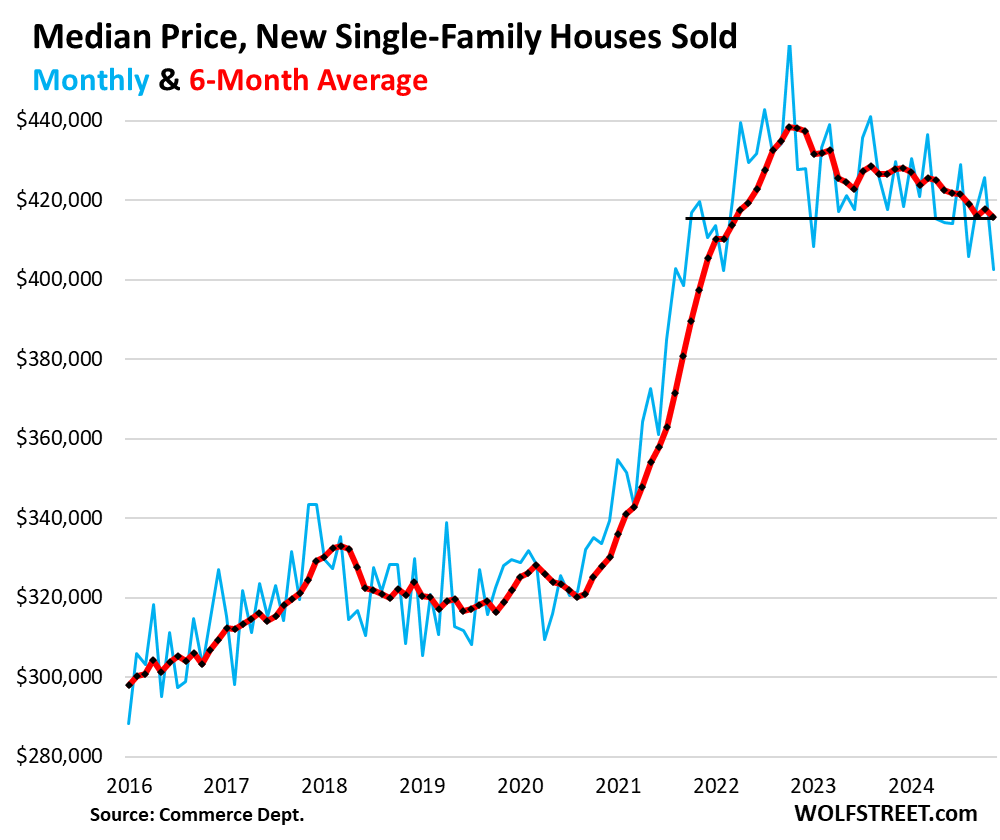

This is the situation that Lennar warned about last week. Homebuilders’ efforts to sell these completed houses will pressure prices down further. The median price in November, reported by the Census Bureau today, which does not include incentives, dropped to the lowest since 2021.

Lennar expects that the average sales price (including incentives) of homes it delivers this quarter will be down by about 16% from two years ago. Lennar’s stock price has tanked by about 28% over the past three months. More on Lennar in a moment.

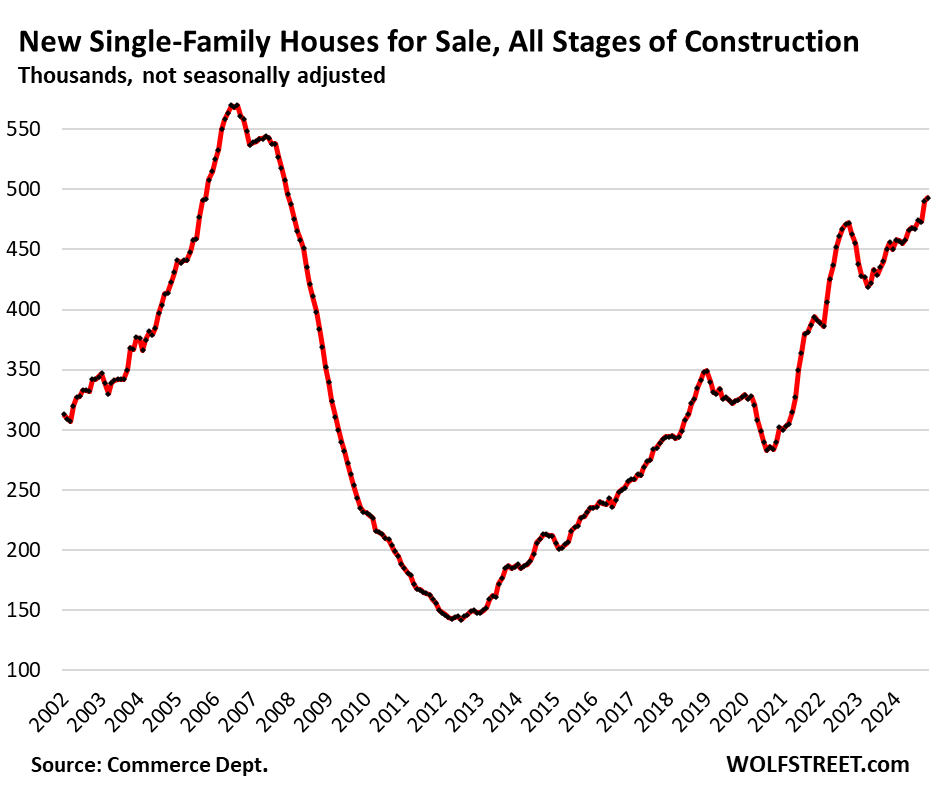

Unsold inventories for sale at all stages of construction – from not yet started to completed – rose by 8.1% from the already bloated levels a year ago, to 493,000 houses, the highest since December 2007. Supply jumped to 9.1 months.

Prices drop, incentives surge.

Big homebuilders cannot sit out this market, they have to build and sell homes because that’s their business, and they have to keep their businesses intact and keep their shares from tanking. So they’re building at lower price points, cutting prices of completed houses, buying down mortgage rates, and throwing in other incentives at a substantial expense to them – just to maintain sales volume by taking share away from homeowners that want to sell an existing property.

Despite the incentives and lower prices, sales volume is now below the targets that the big builders communicated earlier this year, while their incentive costs have jumped, and their margins are getting squeezed. The issue for them is that prices are still way too high, prices have come down, but they haven’t come down nearly enough.

The median contract price of new single-family houses sold at all stages of construction dropped to $402,600 in November, the lowest since September 2021 (blue in the chart below).

The six-month average, which irons out the month-to-month zigzags and includes the revisions, dropped to $415,800, the lowest since March 2022, down by 5.1% from its peak in October 2022.

These contract prices do not include the substantial costs to homebuilders of mortgage rate buydowns and other incentives, though they do include price cuts.

So here comes Lennar, one of the biggest homebuilders in the US. When it reported earnings on December 18 for its fiscal Q4 ended November 30, it dished up a mess:

“Consistent with our strategy of matching sales pace with production, we adjusted sales price, incentives, and margin in order to re-ignite sales and actively manage inventory levels,” it said.

Lennar reported for its fiscal Q4:

- Revenues from home sales fell 9.2% on a 6.7% drop of homes delivered and a 2.5% drop of the average sales price.

- Average sales price of homes delivered fell to $430,000 net of incentives, from $441,000 a year ago, and from $491,000 two years ago.

- Gross margin fell to 22.1%, from 24.2% a year ago, and from 25% two year ago.

- New orders fell by 2.7% to 16,895 homes, 11% below the “low end” of its guidance of 19,000 homes.

A 16% drop in the average sales price (net of incentives) from the peak:

- In fiscal Q3 2022, the average sales price was $491,000, the peak.

- Last quarter, the average sales price was $430,000.

- For the current quarter, Lennar sees $410,000 to $415,000, roughly a 16% drop from Q4 2022.

Gross margin guidance for the current quarter got slashed to 19.0%-19.25%, the lowest since Q2 2018, down from 22.1% last quarter, and down from 25% in Q4 2022, as incentives and lower prices are beginning to bite.

And Lennar said it will not provide gross margin guidance for its full fiscal year “until we have a better sense of market conditions as the year unfolds.”

Sales are decent, thanks to price cuts and incentives.

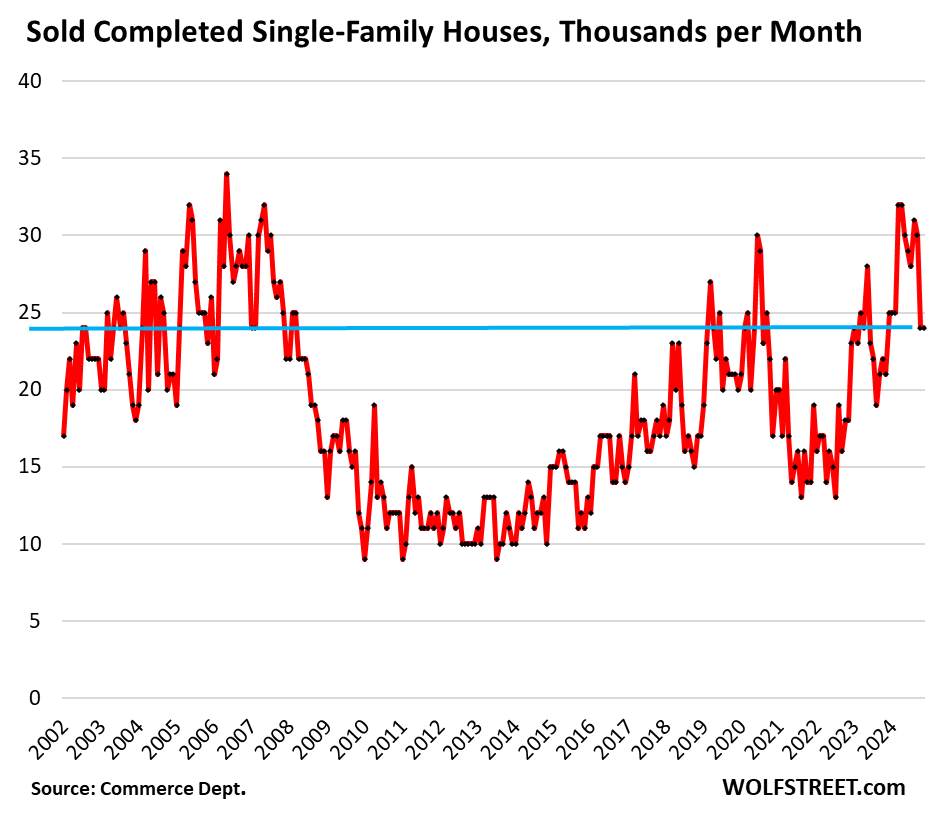

Sales of completed houses – supported by incentives, mortgage rate buydowns, and lower prices – are up about 14% from a year ago, and up 33% from two years ago, to 24,000 houses.

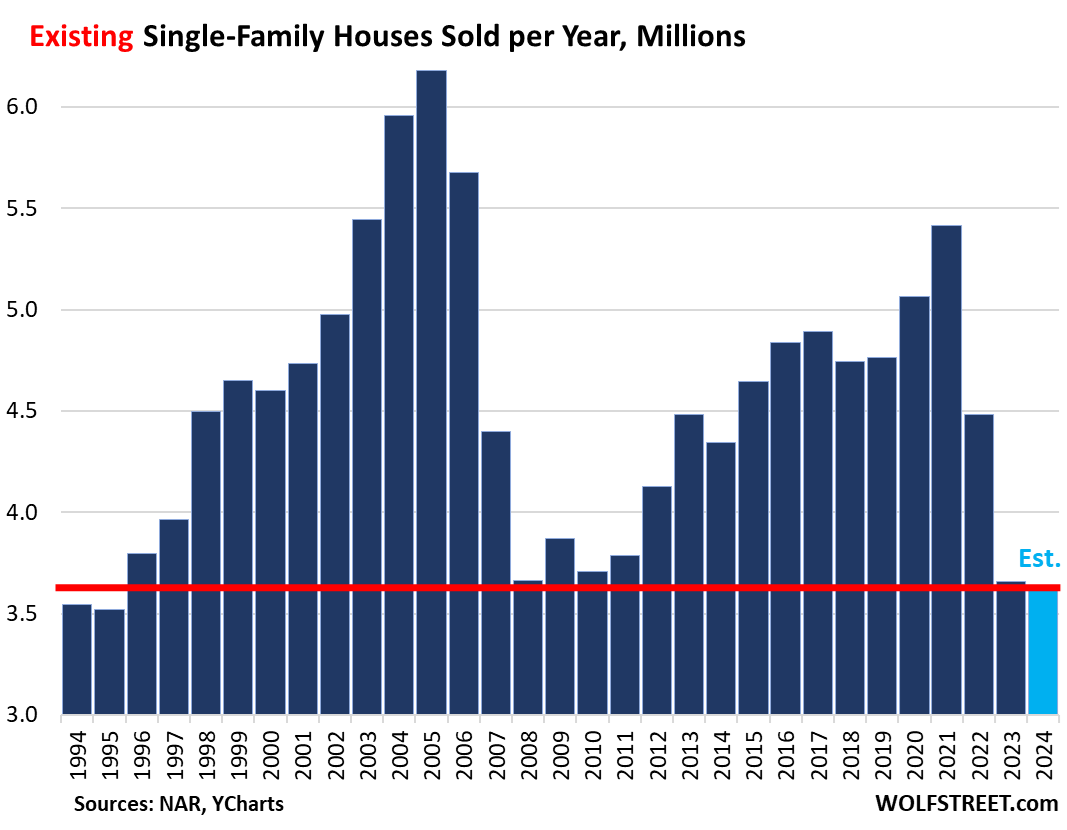

Sales of new houses at all stages of construction, from not started to completed, rose by 7.1% from a year ago, to 45,000 houses. Sales of new houses have been decent, unlike sales of existing single-family houses, where demand has withered because sellers are clinging to those too-high prices.

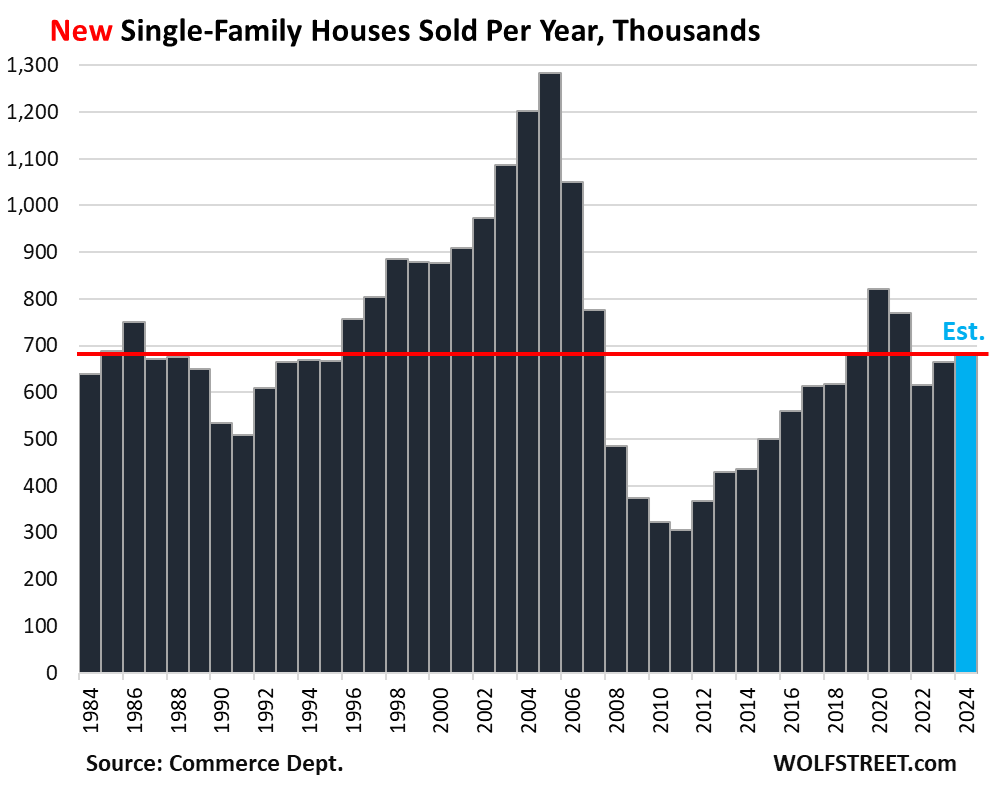

Annual sales of new houses in 2024 – based on the first 11 months of current sales data plus WOLF STREET’s estimate for December – rose slightly to 681,000 houses, a decent level and roughly on par with 2019, and higher than any of the prior 11 years:

By contrast, sales of existing single-family houses in 2024 fell to the lowest level since 1995, according to sales figures by the National Association of Realtors through November plus WOLF STREET’s estimate for December (historical data via YCharts).

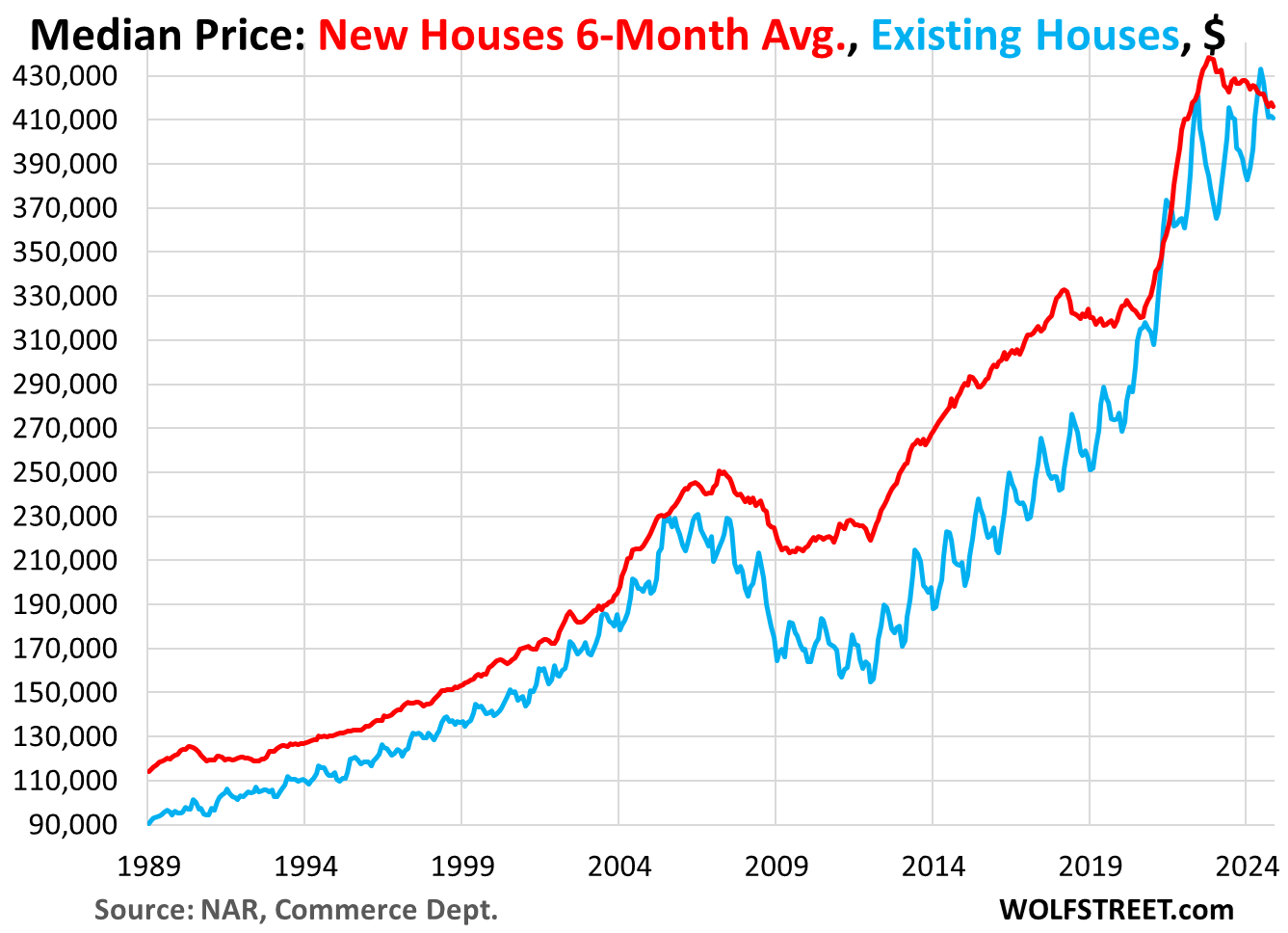

Prices of new houses versus existing houses.

Over the past four decades, the median contract price (six-month average) of new houses exceeded the median price of existing houses nearly all of the time, with new houses being usually 10% to 30% more expensive than existing houses. This scenario has now changed.

And remember, for new houses, the Census Bureau collects contract prices which do not include the incentives and costs of mortgage rate buydowns.

But with mortgage-rate buydowns and other incentives included, the monthly payments of new houses are now out-competing monthly payments of existing houses, which explains why homebuilders’ sales have held up reasonably well, while sales of existing homes have plunged, as some buyers shifted from existing homes to new homes.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Energy News Beat